Strike Price and Fair Market Value: How the Spread Sets Your Tax

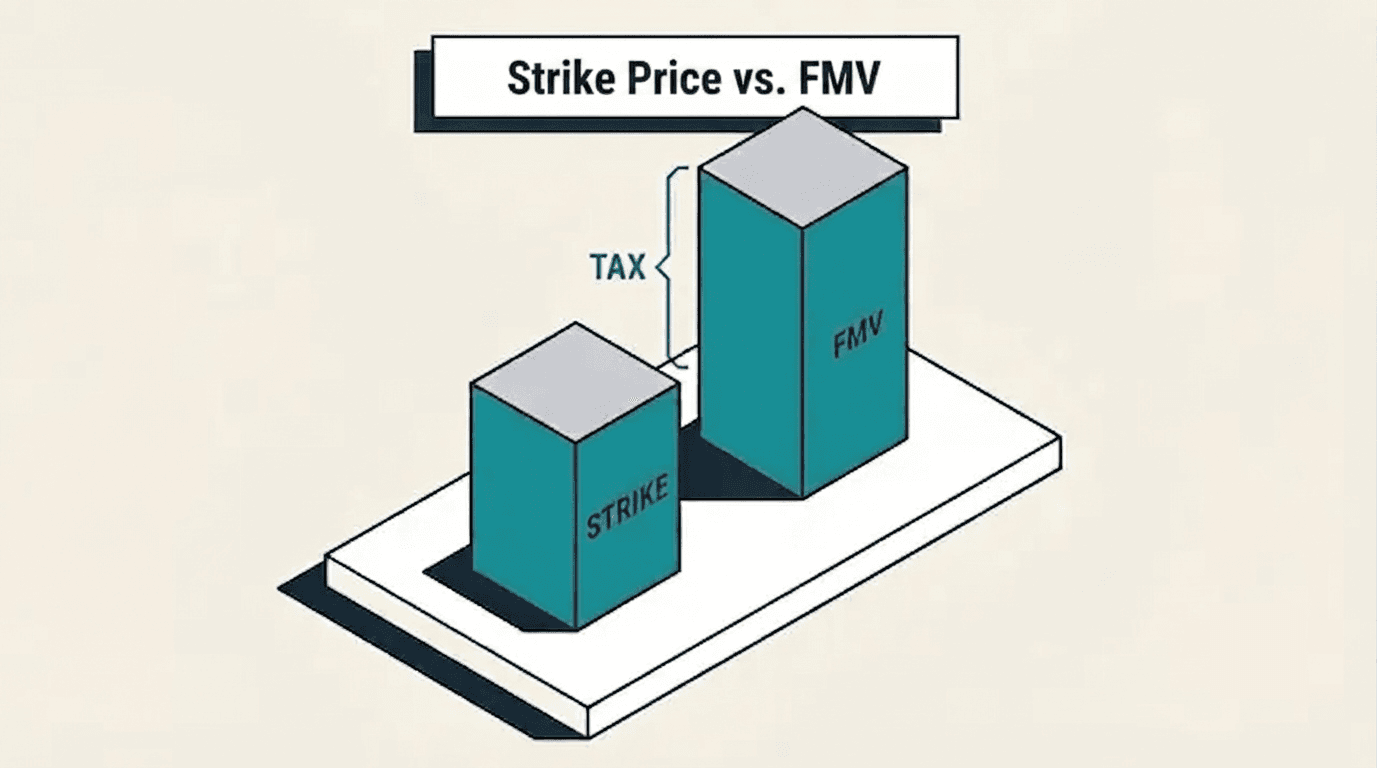

Strike price is what you pay for a share; fair market value is what it's worth today. The gap between them, the spread, is what the IRS taxes.

A strike price is the fixed dollar amount you pay to buy one share under your option grant. Fair market value is what that share is worth right now. The gap between the two, called the spread, is what triggers your tax bill when you exercise, and it grows every time the company's valuation climbs.

Strike price: The fixed price per share written into your option grant. It never changes for the life of that grant.

409A valuation: The independent appraisal that sets the strike price at grant for a private company.

FMV at exercise: What a share is worth on the day you exercise, usually the latest 409A valuation.

The spread: FMV minus strike price. This is the bargain element the IRS uses to calculate your tax.

What sets your strike price at grant

The (also called the exercise price) is the price per share you agree to pay when your option grant is signed. For a private company, that number comes from a , an independent appraisal the company commissions to set the current fair value of its common stock.

The IRS requires the strike price to sit at or above the 409A value at grant. If a company priced options below fair value, employees would receive options already worth more than they cost, which the tax code treats as deferred compensation with its own penalties. Setting the strike at the 409A number keeps a fresh grant at zero built-in value. You aren't handed a gain on day one; you earn one only if the company's value rises after your grant date.

Companies refresh their 409A valuation roughly every twelve months, or sooner after a priced funding round. Every new valuation resets the strike price for grants issued after that date, but it does not touch the strike price on options you already hold. Your strike is locked in at grant and stays there until you exercise or the option expires.

Fair market value at exercise and at sale

is the second number in the equation, and it moves. At a private company, FMV is set by the most recent 409A valuation in effect on the day you exercise. At a public company, FMV is the trading price of the stock at that moment.

FMV also matters again at sale. Once you own the shares, the sale price determines your capital gain or loss, measured against your cost basis rather than your strike price directly. That second FMV, the one on the day you sell, is a separate event from the FMV on the day you exercised, and the two can differ by years and by a wide margin in valuation.

The distinction matters because two different transactions, exercise and sale, each compare your basis against a different market snapshot. Confusing the two is a common source of tax surprises for people exercising options for the first time.

The spread is the number that drives your tax bill

Subtract your strike price from FMV at exercise and you get the spread, also called the bargain element. This is the actual dollar amount the tax code cares about. It represents the value you received for less than it was worth, and every dollar of it eventually shows up on a tax form in one shape or another.

Here is a way to picture it. Your strike price works like a locked-in price on a layaway purchase you arranged months or years ago. Fair market value is today's price tag on that same item at the store. The difference between what you locked in and what it sells for today is the spread, and it exists whether or not you've decided to buy the item yet.

Meet Sana, an engineer at a fictional logistics startup called Lumen Freight. Her option grant carries a $2 strike price. The company's latest 409A valuation puts FMV at $18 per share. If Sana exercises today, her spread is $16 per share; on a grant of 5,000 shares, that's $80,000 of bargain element showing up in the tax calculation the moment she exercises.

A larger spread pushes an ISO exercise further into AMT territory, because the entire spread becomes AMT income in the year you exercise. Sana's $80,000 spread might sit under her AMT exemption in a light income year, or it might tip her straight into the phaseout band in a year when her salary and the spread combine. The size of the spread is the single biggest lever she controls, since she chooses how many shares to exercise and when.

Free tool

See what your spread costs in AMT

Enter your strike price, current FMV, and share count to estimate the AMT a given exercise would trigger, before you commit any cash.

Calculate your AMT exposureISOs and NSOs tax the same spread differently

The spread is identical for both option types on the same grant terms, but the tax code treats it on two completely different tracks.

For an incentive stock option, the spread at exercise is not counted as regular taxable income. Instead, it becomes an preference item, added back into a parallel tax calculation that runs alongside your regular return. You owe no ordinary tax on the spread at exercise, but you may owe AMT, and the size of that bill scales directly with how wide the spread has grown. Our breakdown of the ISO exercise decision walks through how AMT, cash, and concentration risk interact once you're weighing an exercise.

For a nonqualified stock option, the spread at exercise is , full stop. It lands on your W-2 in the year you exercise, your employer withholds against it the same way it withholds against salary, and there's no AMT detour to navigate. The tradeoff for that simplicity is timing: you owe tax the moment you exercise, in cash, regardless of whether the shares are liquid.

This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Neither structure is universally better. NSOs settle the bill immediately and predictably. ISOs defer ordinary tax entirely and open the door to treatment on a qualifying disposition, at the cost of an AMT calculation you have to plan around. Our ISO and NSO guides cover the full mechanics of each, and NSO exercise timing digs into when to pull the trigger on a nonqualified grant.

Why a rising 409A widens the gap over time

Your strike price is frozen the day your grant is signed. Fair market value is not. Every new 409A valuation that comes in higher than the last one widens the spread on the exact same options, without you doing anything at all.

This is why waiting to exercise carries a real cost for ISO holders, even when there's no rush to raise cash. A grant with a $2 strike and a $6 FMV has a $4 spread today. If the next funding round pushes the 409A to $18, that same $2 strike now sits under an $16 spread, and the AMT exposure on a full exercise has roughly quadrupled without a single new share being granted. Employees who exercise early, while the strike and the FMV are close together, lock in a small spread. Employees who wait until the company is close to an IPO often face a spread many times larger on the identical grant.

Our breakdown of how the 2026 AMT rules changed covers how a wider spread interacts with a tighter phaseout band this year specifically, which makes the timing question sharper than it was in prior years.

RSUs skip the strike price entirely

Restricted stock units work on a different mechanism altogether. An RSU carries no strike price and requires no purchase. You're granted the right to receive shares outright, and when they vest, the full fair market value of each share on the vesting date counts as ordinary income, taxed and withheld like salary in that instant.

There's no spread to calculate because there was never a discounted purchase price to compare against. The full share value counts as income at vest. That makes RSUs simpler to model than options, but it also removes the ability to control tax timing the way an option holder can by choosing when to exercise. Our RSU guide covers vesting mechanics and withholding in full.

Common questions

No, not for a compliant grant. The IRS requires a strike price at or above the 409A fair market value on the grant date. A grant priced below that value would create immediate taxable income and trigger penalties under deferred compensation rules, so companies price options at the 409A number specifically to avoid that outcome.

Yes, for ISOs. The AMT preference on an ISO exercise is triggered by exercising, not by selling. You can owe AMT on paper gains from an illiquid private stock you can't yet sell. NSOs work the same way for ordinary income: exercising is the taxable event, regardless of when or whether you sell.

Each grant is priced to the 409A valuation in effect on its own grant date. If the company raised a new round or refreshed its valuation between two grant dates, a later grant can carry a higher strike price than an earlier one, even though both are options in the same company.

Last updated: July 2026. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Consult with an expert

Every funding round widens the spread you'll be taxed on. Waiting rarely makes it cheaper.

No commitment. A clear read on your situation from a CFP® who plans equity compensation for a living.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

This article is for educational purposes only and reflects rules in effect as of the date above. Tax figures are estimates. Consult a qualified tax or financial advisor for advice specific to your situation.

Get the next article in your inbox.

No fluff. Just equity strategy and tax clarity, when it matters.

Keep reading

Incentive stock options (ISO)

How ISOs are taxed, the AMT trap at exercise, and the qualifying-disposition holding periods.

Read the guideCalculatorAMT Safe-Exercise Calculator

Estimate what an ISO exercise could cost you in AMT this year, before you pull the trigger.

Read the guideNSONon-qualified stock options (NSO)

NSOs are taxed as ordinary income at exercise. Timing across tax years is the main lever.

Read the guideImportant disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.