Non-qualified stock options (NSO)

Learn everything you need to know about non-qualified stock options, including how NSOs are taxed at exercise, when to exercise, and how NSOs differ from ISOs.

What are non-qualified stock options?

Non-qualified stock options (NSO) are a type of equity compensation that give employees, contractors, and advisors the right to purchase company stock at a predetermined price, known as a or exercise price. Unlike incentive stock options, NSOs don't have to meet special IRS requirements to qualify for tax treatment, which is what makes them available to a broader group of service providers, not just employees. NSOs are a type of stock option, and are not actual shares of stock. You must exercise your options to become a shareholder.

For recipients, NSOs offer the opportunity to purchase shares at a set price, allowing them to benefit from the stock's appreciation over time. Unlike ISOs, NSOs don't offer any special tax treatment on the spread: the value you capture at exercise is simply taxed as income. An equity compensation advisor can help you decide when to exercise so that spread lands in the tax year that costs you the least, which is the kind of timing decision The Equity Architect works through with clients before shares are exercised, not after.

For companies, NSOs are a flexible way to compensate employees, contractors, board members, and advisors outside of base pay and cash fees. Like ISOs, NSOs are structured with , creating a long-term incentive to stay engaged with the company.

Important terms to know:

: the date a recipient is granted options.

: the fixed price at which a recipient can purchase shares.

: the timeline defining when NSOs can be exercised.

Exercise date: the date on which a recipient purchases shares by exercising NSOs, and the date the taxable spread is measured.

: the difference between the strike price and the fair market value at exercise, always ordinary income for NSOs.

NSO tax treatment

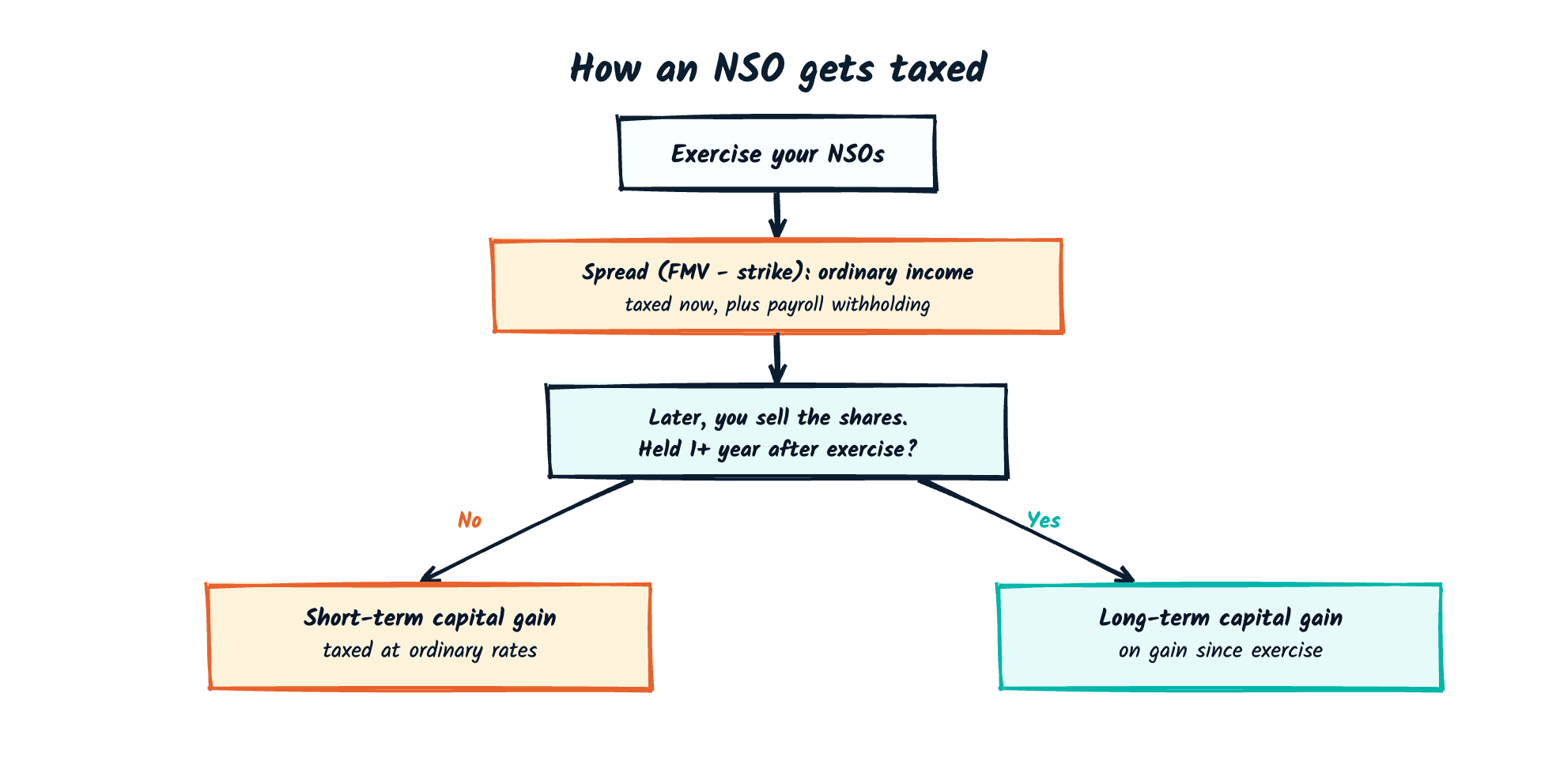

There are two taxable events with non-qualified stock options: the exercise, and the eventual sale of the resulting shares. Unlike ISOs, there is no holding period that converts the exercise spread into a lower tax rate: the spread is always ordinary income, and only appreciation after exercise can qualify for capital gains rates.

Ordinary income at exercise

When you exercise NSOs, the between your strike price and the on the exercise date is added to your W-2 income for that year and taxed at your rate, subject to federal income tax, FICA, and state income tax where applicable. This happens the moment you exercise, whether or not you sell the resulting shares.

The withholding gap

Employers withhold NSO exercise spread at the flat rate: 22% up to $1M in supplemental wages for the year, 37% above it. If your effective tax rate is higher than what was withheld, you carry the difference into the following April, and it can grow with every exercise event.

For example: a hypothetical employee exercises 10,000 NSOs with a $5.00 strike price when the fair market value is $45.00 per share: a $400,000 spread. The employer withholds 22%, or $88,000. If the employee's actual marginal rate on that income is closer to 37%, the real federal liability is around $148,000, a roughly $60,000 shortfall due at tax time, before any state tax.

No AMT on NSO exercise

NSOs are not an preference item. That rule applies only to ISO exercises. If you exercise NSOs, you won't generate an AMT liability from the spread the way you could with ISOs. The tradeoff is that the NSO spread is guaranteed ordinary income at exercise, while an ISO exercise may create no regular tax at all in the year you exercise. If you hold both ISOs and NSOs, it's worth keeping the two separate: our AMT calculator estimates ISO exposure only and doesn't apply to NSO exercises.

A worked example: what an NSO exercise can cost

Consider Maya, a hypothetical single filer and senior engineer who has already earned her $250,000 salary for the year. She holds 20,000 vested NSOs with a $3.00 strike, and the company's fair market value is now $30.00 per share. She decides to exercise all 20,000 and hold, so the long-term capital-gains clock starts.

Maya's NSO exercise, step by step

- Ordinary income at exercise

- ($30 − $3) × 20,000 = $540,000

- Cash to exercise (strike)

- $60,000

- Employer withholds (22% flat)

- ~$118,800

- True federal tax on the spread

- ~$191,800

- Gap owed at filing

- ~$73,000

The 22% supplemental rate withholds about $118,800, but Maya's spread stacks into the 32% to 37% brackets on top of her salary, so her true federal tax is closer to $191,800. That leaves roughly $73,000 owed at filing, before any state tax, plus the $60,000 strike, on shares she cannot sell if the company is still private. Spreading the exercise across tax years, exercising in a lower-income year, or a same-day sale on public shares are the levers that change this math.

Hypothetical, illustrative example. Maya is not a real client and these figures do not represent any actual client or outcome. Numbers are rounded and use approximate 2026 federal figures for a single filer; your result depends on your full tax picture and state. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

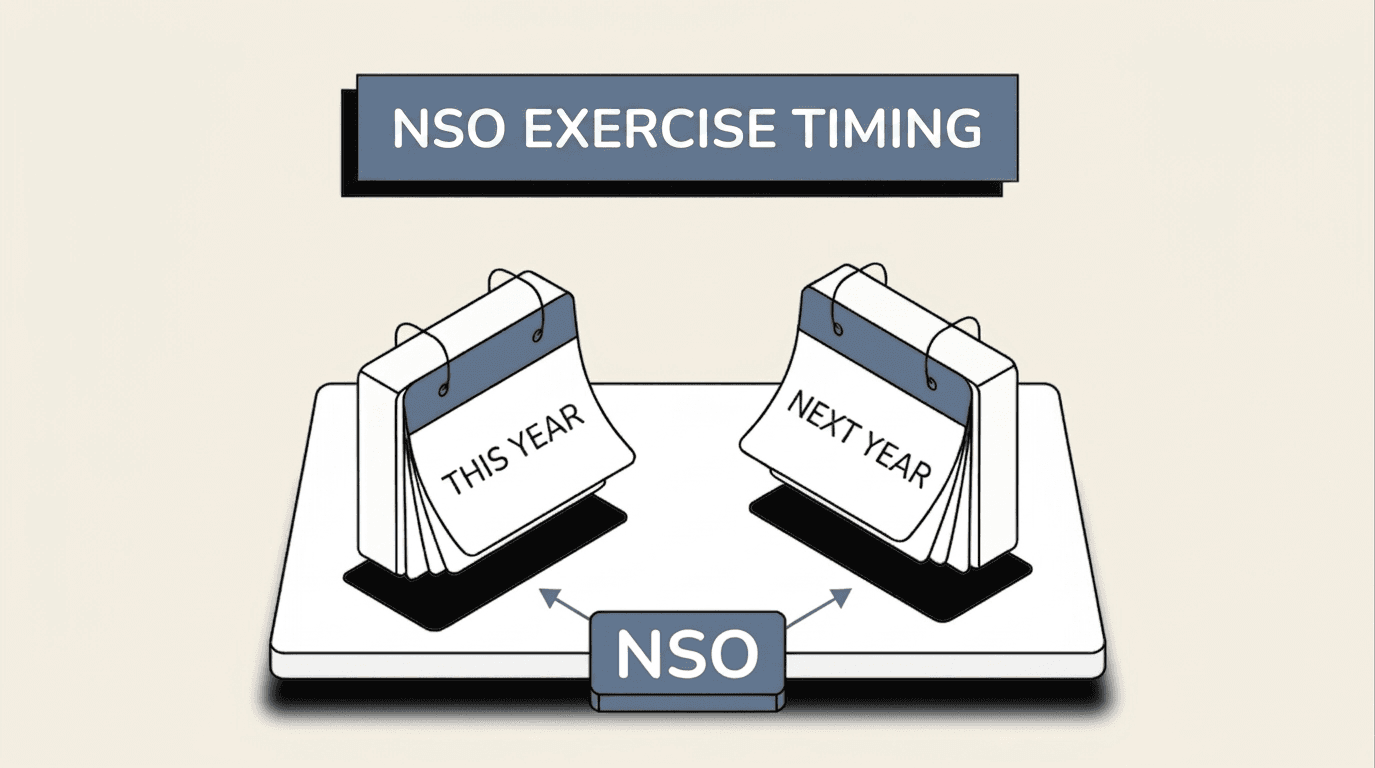

When to exercise NSOs

You can exercise NSOs as soon as they vest, but it's not required. Because the exercise spread is a separate taxable event each time, most plans allow partial exercises: exercising in smaller tranches across multiple tax years is the primary way to manage the ordinary-income spike from a large grant. The tradeoff is that your strike price and expiration date are fixed regardless of when you exercise, so waiting also means carrying market and time-decay risk on the unexercised portion.

In some cases, you might be able to exercise NSOs before they vest. Check your option grant or ask your company if early exercise is allowed. If you early-exercise, filing an within 30 days lets you recognize the (typically small) spread as income immediately, so future appreciation on the shares is taxed at capital gains rates instead of compounding as ordinary income at each later exercise. Consult your tax advisor before early exercising.

NSO expiration and post-termination windows

NSO expiration periods vary by plan: typically anywhere from 90 days to 10 years post-termination. Unlike ISOs, NSOs don't automatically shorten to a 90-day window when you leave a company; the plan document governs, and some employers grant a much longer . Reviewing your option agreement before you leave, not after, is critical, since unexercised NSOs expire worthless once the window closes, regardless of whether the option was ever exercised.

Selling NSO shares

You have to exercise NSOs and purchase shares before you can sell them. Once exercised, the exercise spread has already been taxed as ordinary income: what happens next depends on how long you hold the shares after exercise, not after grant.

If you sell the shares more than 12 months after exercise, any additional appreciation above the fair market value at exercise qualifies for rates. If you sell sooner (including a to cover the cost of exercise, sometimes called a ), any additional gain beyond the already-taxed spread is short-term and taxed at ordinary rates. A same-day sale is lower risk because you haven't invested your own money, but it also means you never hold the position long enough to convert any further upside into capital gains. Not all companies allow cashless exercises, so check with your plan administrator and your tax advisor.

Non-qualified stock options vs. incentive stock options

Incentive stock options (ISO) are the other common type of stock option. ISOs are limited to employees and can qualify for long-term capital gains treatment if specific holding periods are met, but they can also trigger AMT at exercise. NSOs can be granted to employees, contractors, board members, and advisors, and are always taxed as ordinary income at exercise, with no AMT exposure and no special holding-period benefit on the spread itself.

| NSO | ISO | |

|---|---|---|

| Exercise | Ordinary income on the spread | May be subject to alternative minimum tax |

| Sell | Capital gains on post-exercise appreciation | Ordinary income or capital gains |

NSOs vs. equity awards

Instead of stock options, some companies use alternative equity compensation, such as restricted stock awards or restricted stock units (RSU). Both are grants of stock, not options of stock, so there is no strike price and typically no exercise decision to time. RSUs are simply taxed as ordinary income when they vest.

Common questions about NSO taxation

- Non-Qualified Stock Options (NSOs) are taxed as ordinary income at exercise. The spread between the exercise price and the fair market value on the exercise date is added to your W-2 income for the year and subject to federal income tax, FICA, and state income tax.

- ISOs can qualify for long-term capital gains treatment with holding periods and don't trigger AMT on exercise for most employees. NSOs are always taxed as ordinary income at exercise and do not qualify for preferential capital gains treatment on the spread. ISOs are limited to employees; NSOs can be granted to contractors and advisors.

- Yes, but only on appreciation after the exercise date. The spread at exercise is always ordinary income. Post-exercise share price appreciation qualifies for long-term capital gains rates if you hold the resulting shares for more than 12 months before selling.

- NSO expiration periods vary by plan: typically 90 days to 10 years post-termination. Unlike ISOs, NSOs don't automatically shorten to 90 days; the plan document governs. Reviewing your option agreement before leaving is critical, as unexercised NSOs expire worthless once the window closes.

- No. Most plans allow partial exercises. Exercising in smaller tranches across multiple tax years is the primary way to manage the ordinary-income spike, since each exercise is a separate taxable event valued at that day's fair market value. The tradeoff is that the strike price and expiration date are fixed regardless of when you exercise, so waiting also means carrying market and time-decay risk on the unexercised portion.

Supplemental withholding rates per IRS Publication 15. NSO taxation and post-termination treatment per IRS Topic No. 427. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

Consult with an expert

Every NSO exercise is ordinary income, and 22% withholding rarely covers it. Timing is the one lever you control.

Go over your equity, your broader financial goals, and see how the E.Q.U.I.T.Y. System™ can build a plan around them.

Book an Equity Strategy CallMore on Non-Qualified Stock Options

Important disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.