Incentive stock options (ISO)

Learn everything you need to know about incentive stock options, including how ISOs work, AMT exposure, and how ISOs differ from other types of equity.

What are incentive stock options?

Incentive stock options (ISO) are a type of equity compensation that give employees the right to purchase company stock at a predetermined price, known as a or exercise price. ISOs are required to be granted with an exercise price at or above the of the company's common stock on the grant date, making them a popular form of compensation at startups and other fast-growing companies. ISOs are a type of stock option, and are not actual shares of stock. You must exercise your options to become a shareholder.

For employees, ISOs offer the opportunity to purchase shares at a set price, allowing them to take advantage of the stock's appreciation over time. ISOs also carry tax advantages if certain conditions are met, and modeling those conditions before you exercise is exactly the work an equity-comp advisor is there to do with you. The Equity Architect is built around this decision.

For companies, ISOs are a cost-effective way to attract, motivate, and retain talent outside of base pay and bonuses. ISOs are structured with , which creates a long-term incentive for employees to stay with the company.

Important terms to know:

: the date an employee or service provider is granted options.

: the fixed price at which an employee can purchase shares.

: the timeline defining when ISOs can be exercised.

Holding period: the time required for ISOs to qualify for favorable tax treatment.

Exercise date: the date on which an employee purchases shares by exercising ISOs.

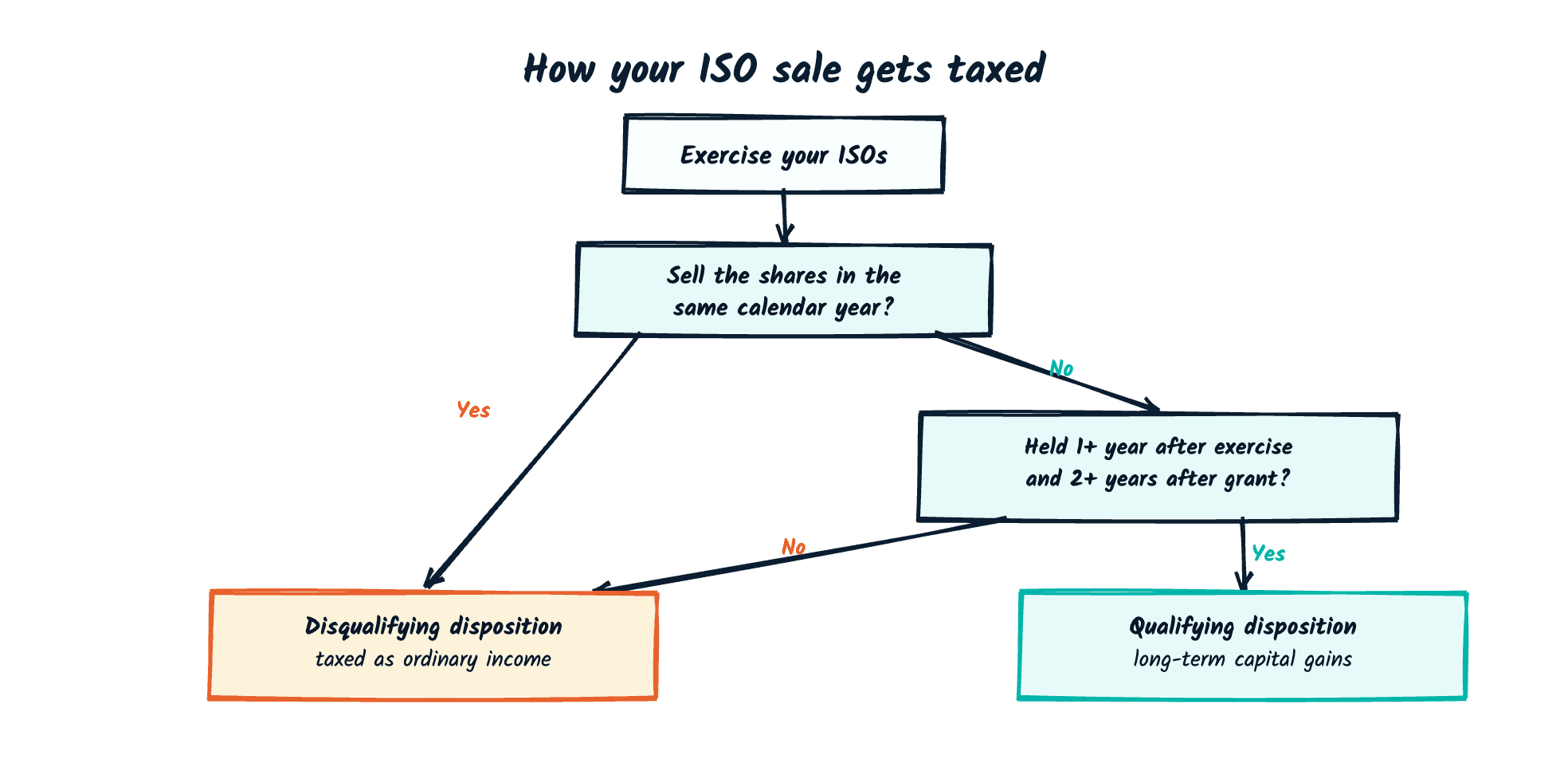

ISO tax treatment

There are two types of taxes to consider with incentive stock options: ordinary income tax and capital gains tax. The capital gains tax rate has historically been lower than the ordinary income tax rate. → Estimate your AMT exposure with our calculator

Qualifying disposition

When you exercise ISOs, you don't have to sell the resulting shares right away. If you exercise ISOs and hold your stock for at least one year after purchase and two years after grant, your stock should be eligible for a : favorable tax treatment when you sell, taxed at the lower capital gains rate. However, you may be subject to the alternative minimum tax (AMT) when you exercise.

The alternative minimum tax and ISOs

The is a parallel way of calculating your federal tax. You figure your tax the regular way, figure it again under AMT rules, and pay whichever is higher. When you exercise ISOs and hold the shares past the end of the year, the counts as income under the AMT calculation even though you have not sold anything. That is why ISO exercises can trigger a tax bill on gains you cannot yet touch.

For 2026 the AMT exemption is $90,100 for single filers and $140,200 for married couples filing jointly, per the IRS 2026 inflation adjustments. The exemption starts to phase out once AMT income passes $500,000 (single) or $1,000,000 (joint), and under the One Big Beautiful Bill Act it now phases out at 50 cents per dollar rather than 25. A large ISO exercise pushes most senior tech earners well into that phase-out, so the exemption often disappears entirely.

Two facts change how this feels. First, exercising and selling in the same calendar year converts the spread to ordinary income for regular tax, which removes the AMT preference and the phantom bill along with it. Second, AMT you pay on an ISO exercise usually becomes a minimum tax credit that carries forward and comes back to you in later years when your regular tax exceeds your AMT, sometimes over several years and not always in full. For most people the AMT on an exercise-and-hold is a timing cost, not a permanent one. It still has to be paid in cash the year you exercise.

The pre-IPO lever

The AMT preference is the spread at exercise. Exercising early, while your strike and the 409A fair market value are still close, can make that spread small enough that the AMT is minimal. Exercising early also starts your capital-gains and, if the stock qualifies, holding clocks, which run from the exercise date, not the grant date. Waiting until the 409A steps up after a financing round can turn a manageable exercise into a six-figure AMT bill.

The $100K ISO limit

The $100,000 limit caps how much of your equity keeps ISO treatment in a single year. Only $100,000 of stock, measured by fair market value at grant, can become exercisable for the first time in any calendar year and still count as an ISO. Anything above that line is treated as a non-qualified stock option by law, no matter what your grant paperwork says. Large grants at low-strike startups cross this line more often than employees expect, so it is worth checking your Form 3921 and broker records rather than assuming every option is an ISO.

Free tool

See how the $100K limit affects your exercise

Run your own numbers through our free AMT calculator to see how many shares you can exercise before the $100K limit and AMT exposure start working against you.

Try the AMT calculator

Disqualifying disposition

If you sell shares exercised from ISOs right away (for example, to cover the cost of exercise), the shares you sell won't qualify for favorable tax treatment. Instead, this is a : taxed like non-qualified stock options, with ordinary income tax on the spread between your strike price and the FMV at the time of sale.

A worked example: what an ISO exercise can cost

Numbers make the AMT risk concrete. Consider Priya, a hypothetical single filer and senior engineer at a pre-IPO company. She earns $240,000 in salary and holds 40,000 vested ISOs with a $2.00 strike. A recent 409A valuation puts the fair market value at $22.00 per share. She is deciding whether to exercise all 40,000 shares and hold them.

Priya's exercise-and-hold, step by step

- Bargain element (AMT preference)

- ($22 − $2) × 40,000 = $800,000

- Approximate AMT income

- ~$1,040,000

- AMT exemption after phase-out

- $0

- Tentative minimum tax

- ~$286,000

- Regular tax

- ~$48,000

- Extra AMT owed in cash

- ~$238,000

To exercise and hold, Priya needs the $80,000 strike cost plus roughly $238,000 of AMT in cash this year, on stock she cannot sell because the company is still private. Most of that AMT returns to her later as a minimum tax credit, but the cash leaves her account now, and it rides on a liquidity event that has not happened yet.

This is the moment the levers matter. Exercising a smaller tranche each year, up to the point where the AMT just begins, spreads the cost across tax years. Exercising early on her next grant, before the 409A steps up, would shrink the spread and the AMT with it. And a same-day sale would remove the AMT entirely, at the cost of ordinary-income treatment and no path to long-term capital gains. Which lever fits depends on her cash, her conviction in the company, and how much of her net worth is already tied to it. Run your own numbers through the AMT calculator to see where your crossover sits.

Hypothetical, illustrative example. Priya is not a real client and these figures do not represent any actual client or outcome. Numbers are rounded and use approximate 2026 federal figures for a single filer; your result depends on your full tax picture. Reconcile any exercise against a live calculation and the current Form 6251 instructions. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

When can I exercise ISOs?

Usually, you can't buy all of your shares right away and have to work for the company over time to be able to purchase your shares. This process is called vesting. You can exercise your ISOs as soon as your options have vested, but it's not required.

Some plans let you exercise ISOs before they vest. If yours does, and you exercise early, you can file an within 30 days. For an ISO the 83(b) election works only for AMT: it locks the AMT spread at the exercise-date value so it is not re-measured, and usually higher, as each tranche vests. It has no effect on your regular tax. Early exercise plus an 83(b) election is one of the strongest ways to keep AMT low on a fast-appreciating startup, but the 30-day window is firm and the cash goes in before the shares are yours to keep, so weigh it with a tax advisor before you file.

When do incentive stock options expire?

Theoretically, ISOs have an expiration date of 10 years from the date you're granted them. However, your company might enforce a that gives you a shorter amount of time to exercise options after you leave the company. If you don't exercise them before that period ends, you may lose the opportunity to purchase them.

Leaving a company starts a separate clock that no employer can extend. Under the tax code, an option keeps ISO treatment only if you exercise while employed or within three months of your last day. On day 91 the option becomes a non-qualified stock option by law. Some companies now offer long post-termination windows, up to ten years, but any exercise past the three-month mark is an NSO exercise with ordinary income on the spread, not an ISO. For a departing senior employee holding a large, in-the-money ISO, that compresses a six-figure cash-and-AMT decision into 90 days, often on stock that is still private. It is one of the highest-stakes moments in an equity package and the easiest to miss.

When can I sell my ISOs?

You have to exercise ISOs and purchase shares before you can sell them. If you choose to exercise your ISOs, you usually have two options: pay for the total in cash, or do a “same-day sale”: sell a portion of your shares to cover the cost of exercise.

Selling to cover exercise costs is called a . It carries less risk because you have not committed your own cash, but selling right after exercising gives up the ISO tax structure. Not all companies allow cashless exercises, so check with your plan administrator and your tax advisor.

The real decision sits between two paths. A same-day sale gives you liquidity now and no AMT, but the spread is taxed as ordinary income and no holding clock starts. Exercise-and-hold opens the door to long-term capital gains and QSBS, but you take on AMT exposure and you hold concentrated, often illiquid, stock in a single employer. That last point matters more than the tax rate. Exercising and holding pre-IPO shares can leave you with a real cash AMT bill on paper gains you cannot sell, and if the company later falls, you may have paid tax on value that never arrived. Let the tax treatment inform the decision, not drive it. How much of your net worth belongs in one company's stock is the question that comes first.

Incentive stock options vs. non-qualified stock options

Non-qualified stock options (NSO) are another type of stock option companies may offer to employees. With NSOs, you pay taxes both when you exercise and when you sell your options, usually meaning you pay more taxes with NSOs than with ISOs.

| ISO | NSO | |

|---|---|---|

| Exercise | May be subject to alternative minimum tax | May be subject to ordinary income tax |

| Sell | Ordinary income or capital gains | Capital gains |

ISOs vs. equity awards

Instead of stock options, some startups use alternative equity compensation, such as restricted stock awards or restricted stock units (RSU), depending on the company's stage. Both are grants of stock, not options of stock, so you typically don't need to exercise them.

Common questions about ISO taxation

- When you exercise ISOs, the spread between the strike price and the fair market value at exercise is an AMT preference item. If the resulting AMT exceeds your regular tax liability, you owe the difference, often on stock you have not yet sold. This is the primary risk of ISO exercises at high valuations.

- A qualifying disposition occurs when you hold ISO shares for more than 2 years from the grant date AND more than 1 year from the exercise date. Gains from a qualifying disposition are taxed at long-term capital gains rates (0%, 15%, or 20%) rather than ordinary income rates.

- To keep ISO treatment, you must exercise while employed or within three months of your last day. On day 91 an unexercised ISO becomes a non-qualified stock option by law, even if your company offers a longer post-termination window. Exercising after the three-month mark still buys the shares, but the spread is taxed as ordinary income rather than qualifying for ISO treatment.

- The $100,000 ISO limit applies to the aggregate fair market value of ISOs that first become exercisable in any calendar year, measured at each grant's grant date. Anything above $100,000 is automatically treated as a non-qualified stock option, regardless of what your grant says. Large grants at low-strike startups cross this line more often than employees expect.

- Not always, but you can often minimize it. Exercising fewer shares in a calendar year, spreading exercises across multiple years, or exercising early when the strike-to-FMV spread is small (before a 409A step-up) can keep your AMT preference income under the exemption. For 2026 the AMT exemption is $90,100 for single filers and $140,200 for joint filers, and it phases out above $500,000 and $1,000,000 of AMT income. AMT paid on an exercise usually returns later as a minimum tax credit, though it does not solve the up-front cash-flow problem of an illiquid bill.

- Yes. The qualified small business stock (QSBS) holding period runs from the exercise date, when you acquire the shares, not from the grant date. Exercising early can move you toward the QSBS exclusion sooner. For stock issued after July 4, 2025, the One Big Beautiful Bill Act phases the exclusion in at 50% after three years, 75% after four, and 100% after five.

- When you exercise and hold ISOs, the spread between your strike and the fair market value counts as income under the AMT calculation even though you have not sold anything. At a pre-IPO company that can produce a real cash AMT bill on paper gains with no way to sell shares to pay it. This illiquid-AMT risk is the main reason to model an exercise before committing the cash.

AMT exemption and phase-out amounts per IRS annual inflation adjustments. ISO qualifying-disposition and post-termination rules per IRS Topic No. 427 and the Form 6251 Instructions. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

Consult with an expert

Exercise ISOs without a plan and AMT can tax you on gains you never sold. The safe number moved for 2026.

Go over your equity, your broader financial goals, and see how the E.Q.U.I.T.Y. System™ can build a plan around them.

More on Incentive Stock Options

83(b) Elections: The 30-Day Filing That Can Save Six Figures

An 83(b) election taxes restricted stock or early-exercised options at today's low value instead of at each vesting date, starting the capital gains and QSBS clocks early. The filing deadline is 30 days from exercise, with no extensions.

The ISO Exercise Decision: AMT vs. Cash-Flow Tradeoffs

Exercising incentive stock options means weighing an AMT bill, the cash to exercise, and concentration risk together, not solving for AMT alone. Here is how the three factors interact.

Strike Price and Fair Market Value: How the Spread Sets Your Tax

Strike price is what you pay for a share; fair market value is what it's worth today. The gap between them, the spread, is what the IRS taxes.

Important disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.