The ISO Exercise Decision: AMT vs. Cash-Flow Tradeoffs

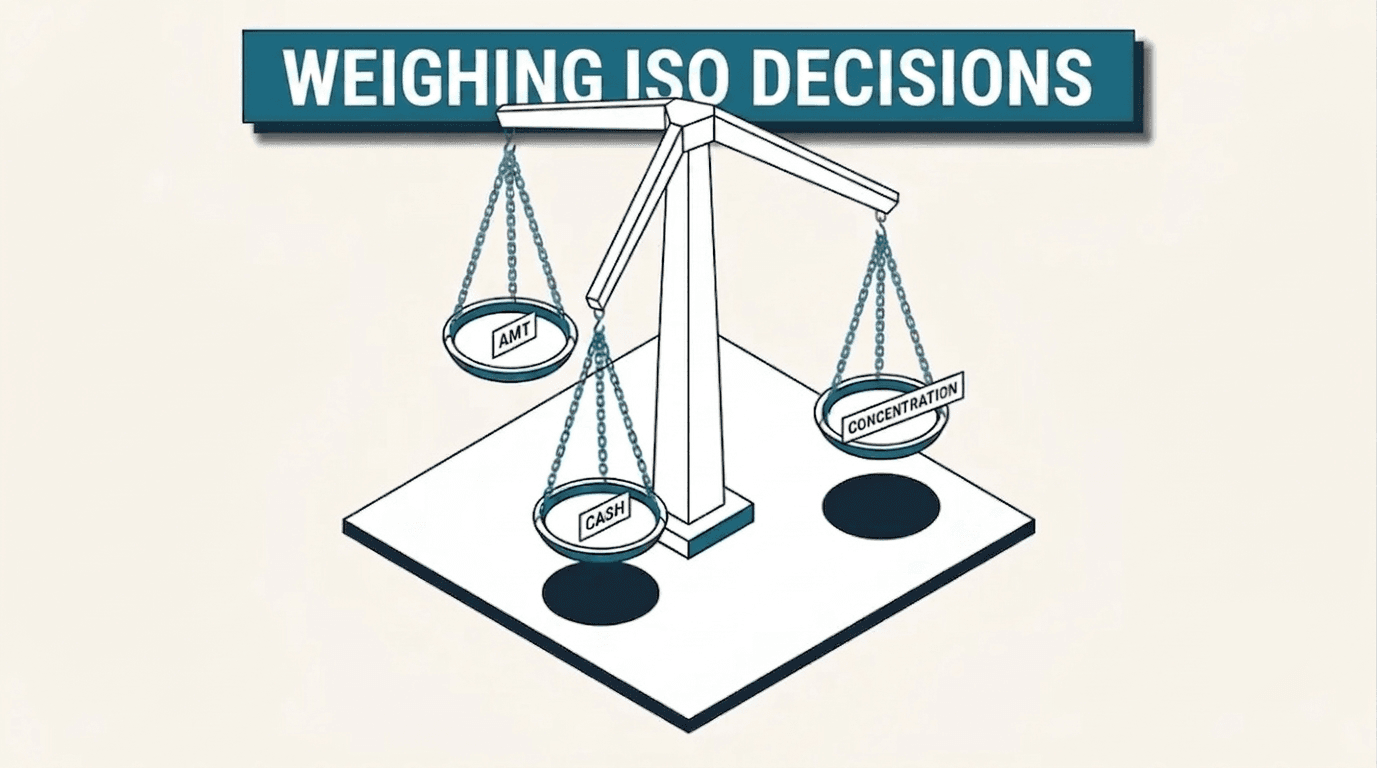

Exercising incentive stock options means weighing an AMT bill, the cash to exercise, and concentration risk together, not solving for AMT alone. Here is how the three factors interact.

Exercising incentive stock options creates three separate costs at once: an AMT bill on paper gains you haven't collected, cash you send the company before you own a single share, and a concentrated bet on one private stock. The right exercise decision weighs all three together. Treating it as a pure AMT calculation misses the cash-flow and concentration risk that matter just as much.

Exercising ISOs is a three-way tradeoff

An problem is the loudest part of an ISO exercise, but it is one leg of a three-legged decision. The other two legs are the cash required to pay the , and the concentration risk of holding a large, illiquid stake in a single private company after you exercise.

The , the spread between the current fair market value and your exercise price, drives the AMT calculation. A wide spread on a large grant can generate a tax bill in the tens or hundreds of thousands of dollars, due the April after you exercise, even though you cannot sell a single share to raise the cash. Employees who focus only on that number miss two things that matter just as much: whether they have cash outside the brokerage account to cover the exercise cost and the AMT together, and what a 40% drop in the company's valuation before a liquidity event would do to their net worth.

Ignoring any one leg produces a bad outcome. An employee who solves for the lowest AMT bill by exercising a small number of shares each year may end up holding almost nothing when the company finally goes public. An employee who exercises everything to start the capital gains clock may tie up six figures in cash and stock with no way to sell for years, sometimes in a company that never reaches a liquidity event at all. For the mechanics behind grants, vesting, and the $100,000 ISO limit, our ISO guide covers the fundamentals this article builds on.

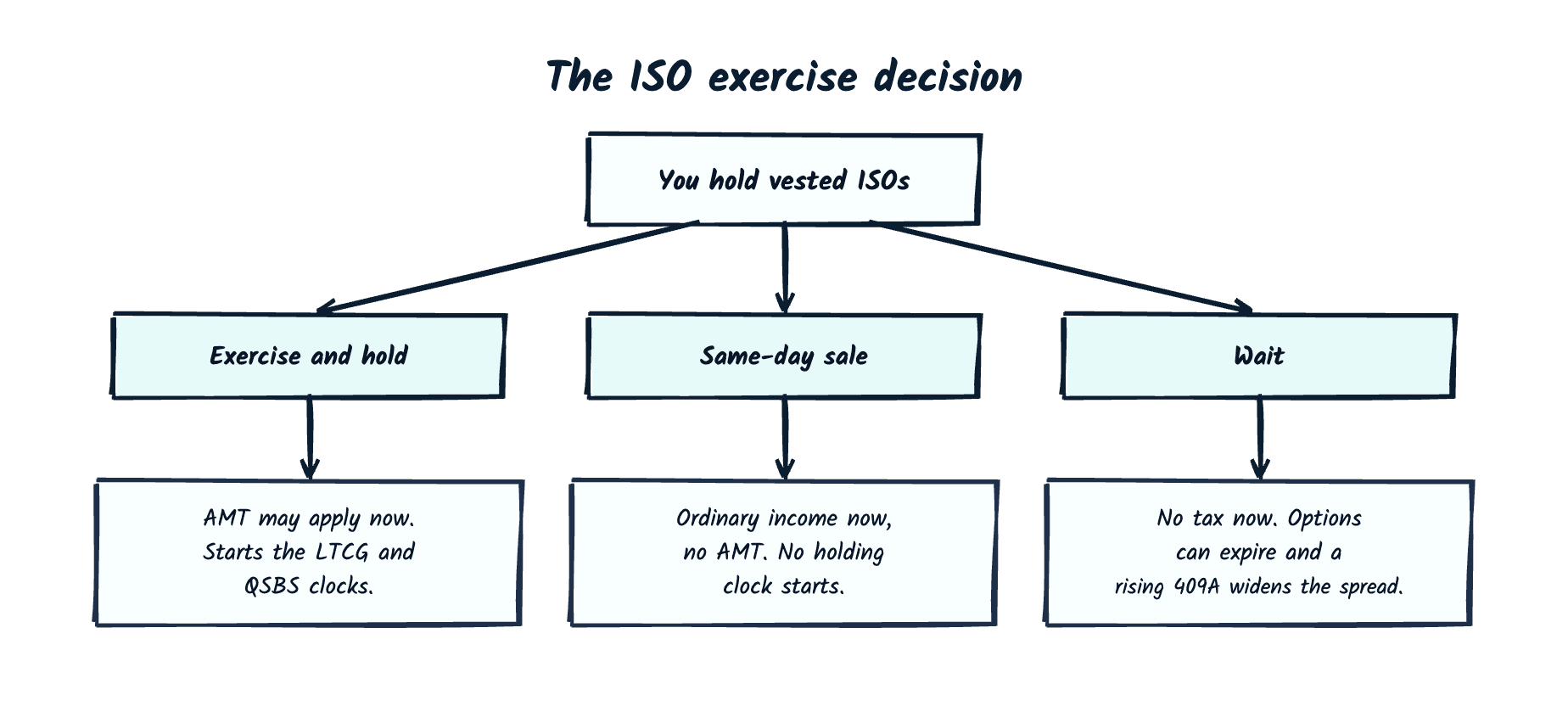

Exercise-and-hold and same-day sale solve different problems

A same-day sale exercises and sells the shares in the same transaction, converting the entire bargain element into ordinary income as a . No AMT applies to a same-day sale because the ISO's special tax treatment never kicks in; the IRS taxes it like a nonqualified option instead. That makes same-day sale the simplest path, and it works well when you want the cash, when the company is already public with a liquid market, or when the AMT math on a full exercise-and-hold would be punishing relative to your income.

Exercise-and-hold means paying the exercise price, taking the shares into your brokerage account, and holding rather than selling right away. This path preserves the possibility of a , which requires holding the shares more than one year from exercise and more than two years from grant. A qualifying disposition converts the full gain to long-term capital gains rates instead of ordinary income, and it is the only path that starts the clock toward a Section 1202 QSBS exclusion if the underlying company qualifies. The cost of that upside is the AMT and the cash tied up in an illiquid position for however long it takes the company to reach a liquidity event.

Most people who exercise ISOs at a private company don't choose one path for every share. A common approach exercises a portion for the AMT-favorable spread and holding period, while planning a same-day or near-term sale for the rest once the company goes public and stock becomes liquid.

The AMT crossover shows where exercising gets expensive

The AMT system runs a second, parallel tax calculation that adds the ISO bargain element back into income, then applies its own exemption, phaseout, and rate structure. For 2026, the AMT exemption is $90,100 for single filers and $140,200 for those married filing jointly. The exemption phases out at 50 cents per dollar of AMT income above $500,000 single or $1,000,000 married, up from 25 cents under prior law, which pushes the effective marginal rate in the phaseout band to roughly 42%. Above the exemption, AMT income is taxed at 26% up to $244,500 and 28% on the amount above that threshold.

The "crossover" is the point where your regular tax and your tentative minimum tax cross, and it turns on your regular income, filing status, and the size of the bargain element you add through exercise. A modest exercise against a large regular income might generate no AMT liability at all, because your regular tax already exceeds the tentative minimum tax. A large exercise against a modest regular income can generate a substantial AMT bill because the bargain element pushes your AMT income well past your regular taxable income.

This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Every year's crossover point moves with the exemption, phaseout thresholds, and your own income, which is why the 2026 rule changes matter for anyone planning an exercise this year. See our breakdown of the 2026 AMT rule changes for how the higher phaseout rate reshapes the math for higher earners.

The cash you need up front is separate from the AMT bill

Exercising an ISO requires two potential cash outlays that arrive on different timelines. The first is the exercise price itself, due to the company at the moment you exercise: shares times your strike price, payable in cash unless your plan permits a net exercise or cashless structure. The second is the AMT liability, which doesn't come due until you file your tax return the following spring, but which you need to plan for well before then.

Both outlays happen before you can sell a single share if you're exercising and holding at a private company. That combination catches people off guard. They budget for the exercise price, forget that the AMT bill can be several times larger, and end up scrambling to find cash or selling other assets at an inconvenient time.

If you're weighing an early exercise of unvested ISOs, a different clock applies: an 83(b) election must be filed within 30 days of the exercise, with no extensions and no reversal once filed. Our 83(b) election deadline guide walks through that filing in detail. It's a separate decision from the standard post-vesting exercise this article covers, but the two come up together for early employees.

Free tool

What's your AMT number?

Run your grant details through our free calculator to see the AMT impact of exercising some, or all, of your vested ISOs before you commit cash to the decision.

Try the AMT calculator

Holding starts the long-term capital gains and QSBS clocks

A qualifying disposition only happens if you hold the shares more than one year past exercise and more than two years past grant, and hitting both dates is what converts the gain from ordinary income to long-term capital gains rates. Selling one day early on either clock triggers a disqualifying disposition and pushes some or all of the gain back to ordinary income treatment, even if you held the shares for years.

Holding also starts the clock toward a exclusion under Section 1202, if the company itself qualifies as a small business under that section. Stock acquired on or before July 4, 2025 needs a full five-year hold for a 100% exclusion, capped at the greater of $10 million or 10 times basis, with a $50 million gross-assets test measured at issuance. Stock acquired after July 4, 2025 follows a tiered schedule instead: 50% excluded at three years, 75% at four years, and 100% at five years, with a raised $15 million cap and a $75 million gross-assets test. The non-excluded portion of gain on the newer stock is taxed at a flat 28% rate. California does not conform to either regime and taxes the full gain regardless of hold period.

The QSBS clock only starts running once you exercise and own the shares outright. Options you haven't exercised don't count toward the holding period, which is one of the strongest arguments for exercising early at a company you believe in and can afford to hold, rather than waiting until an IPO is imminent and the stock is worth far more.

A worked example: Priya's exercise decision

Priya is a staff engineer at Vantia Robotics, a pre-IPO climate-tech company. She holds 20,000 vested ISOs with a $3 exercise price. The company's latest 409(a) valuation puts fair market value at $18 per share, so exercising all 20,000 options costs $60,000 in cash and creates a bargain element of $300,000 ($15 spread times 20,000 shares).

Priya earns $180,000 in salary. Adding $300,000 of AMT income from the bargain element pushes her tentative minimum tax calculation well above her regular tax liability for the year, generating an AMT bill that could run into the tens of thousands of dollars depending on her other deductions and income. That bill is separate from the $60,000 exercise cost, and both compete for the same pool of savings.

Priya decides to exercise 8,000 shares this year, a partial exercise that costs $24,000 in cash and keeps the bargain element small enough that her AMT exposure stays manageable. It works like buying a long-term CD: she locks up cash today, and the bigger payout only arrives if she leaves it in place until the term matures instead of cashing out early. She plans to exercise the remaining 12,000 shares in a future year, spreading the AMT impact across two tax years instead of concentrating it in one. If Vantia goes public and she holds her exercised shares past the one-year and two-year marks, she qualifies for long-term capital gains treatment on the sale, and if Vantia meets the QSBS gross-assets test, a meaningful portion of her gain could be excluded from tax entirely. If she leaves Vantia before then, she has 90 days to exercise any remaining vested options before they convert to nonqualified status under the standard , and unexercised ISOs expire completely 10 years from grant regardless.

A simple framework for deciding how many ISOs to exercise

Start with the AMT number before the cash number. Run your specific grant details, exercise price, current fair market value, and shares outstanding, through a calculator built for this, since a spreadsheet estimate rarely captures the phaseout math correctly. Then work through cash, timing, and risk in order.

Size the AMT exposure first. Know the dollar figure before you decide how many shares to exercise. Splitting the exercise across two tax years keeps the bargain element under the level that triggers meaningful AMT.

Confirm the cash is separate from your emergency fund. Budget for the exercise price and the following year's AMT bill as two distinct outlays, both due before you can sell a single share.

Check your concentration risk after exercise. Add up what the exercised shares would be worth at current fair market value and compare that number to your total net worth. A position worth more than 15-20% of your net worth in one illiquid private stock carries real regardless of the tax math.

Watch your departure timeline. If you might leave the company, the post-termination exercise window forces a faster decision than the tax clocks do, since a departure starts a 90-day countdown on any options you haven't exercised.

None of these four steps override the others. A low AMT bill doesn't make a position worth 40% of your net worth in one private company a good idea, and a favorable concentration profile doesn't make an unaffordable AMT bill worth taking on. Weigh the AMT bill, the cash required, and the concentration risk together before you commit money.

Common questions

Rarely, for shares with a large bargain element. Exercising in stages across two or more tax years spreads the AMT income so each year's tentative minimum tax stays closer to your regular tax, reducing the total AMT owed compared to one large exercise. It also spreads out the cash requirement. The tradeoff is that shares exercised later start their long-term capital gains clock later too, so staging works best when you aren't racing a known liquidity event.

You still owe the AMT for the year you exercised, even though the shares stay illiquid and could end up worth nothing. The AMT you paid becomes a minimum tax credit that carries forward with no expiration date, usable in a future year when your regular tax exceeds your tentative minimum tax. That credit doesn't return your cash immediately, and if the company fails, you may never fully recover the AMT paid, which is the core argument for sizing any exercise against your ability to absorb a total loss on that position.

It can, but only if the issuing company meets the Section 1202 requirements, including the gross-assets test measured at the time your shares were issued, and only after you satisfy the holding period. Stock acquired after July 4, 2025 needs at least three years for a partial exclusion and five years for the full amount; stock acquired earlier needs a full five years for any exclusion at all. Ask the company whether it has confirmed QSBS eligibility, and confirm your own state's conformity, since California taxes the gain in full either way.

Last updated: July 2026. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Consult with an expert

Fixate on the AMT bill alone and the cash and concentration risk will blindside you.

No commitment. A clear read on your situation from a CFP® who plans equity compensation for a living.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

This article is for educational purposes only and reflects rules in effect as of the date above. Tax figures are estimates. Consult a qualified tax or financial advisor for advice specific to your situation.

Get the next article in your inbox.

No fluff. Just equity strategy and tax clarity, when it matters.

Keep reading

Incentive stock options (ISO)

How ISOs are taxed, the AMT trap at exercise, and the qualifying-disposition holding periods.

Read the guideCalculatorAMT Safe-Exercise Calculator

Estimate what an ISO exercise could cost you in AMT this year, before you pull the trigger.

Read the guideNSONon-qualified stock options (NSO)

NSOs are taxed as ordinary income at exercise. Timing across tax years is the main lever.

Read the guideImportant disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.