Restricted stock units (RSU)

Learn how RSUs are taxed, why the default withholding almost never covers the bill, and how to manage the concentration risk that comes with every vest.

What are restricted stock units?

Restricted stock units (RSU) are a promise from your employer to deliver shares of company stock once a set of conditions (typically continued employment over time) has been met. Unlike stock options, RSUs are an outright grant of stock, not a right to purchase it. There is no to pay: once your RSUs vest, the shares are simply yours.

For employees, RSUs are simpler to understand than options: there is no decision about whether or when to exercise, and no risk of a grant expiring worthless if the stock price falls below a strike price. The tradeoff is timing. Because RSUs are taxed the moment they vest rather than when you choose to sell, you have less control over when the tax bill arrives, which is exactly why RSU tax planning matters more than most people expect. The Equity Architect builds that planning around your actual vesting schedule, not a generic withholding assumption.

For companies, RSUs have become the dominant form of equity compensation at public and late-stage private companies, largely replacing stock options as the default grant type for established tech employers.

Important terms to know:

: the date an employee is granted RSUs.

: the timeline defining when RSUs convert to shares you own.

Vest date: the date shares are delivered and the taxable event occurs.

: the share price on the vest date, which sets both your taxable income and your cost basis.

: the flat IRS withholding rate applied to RSU income.

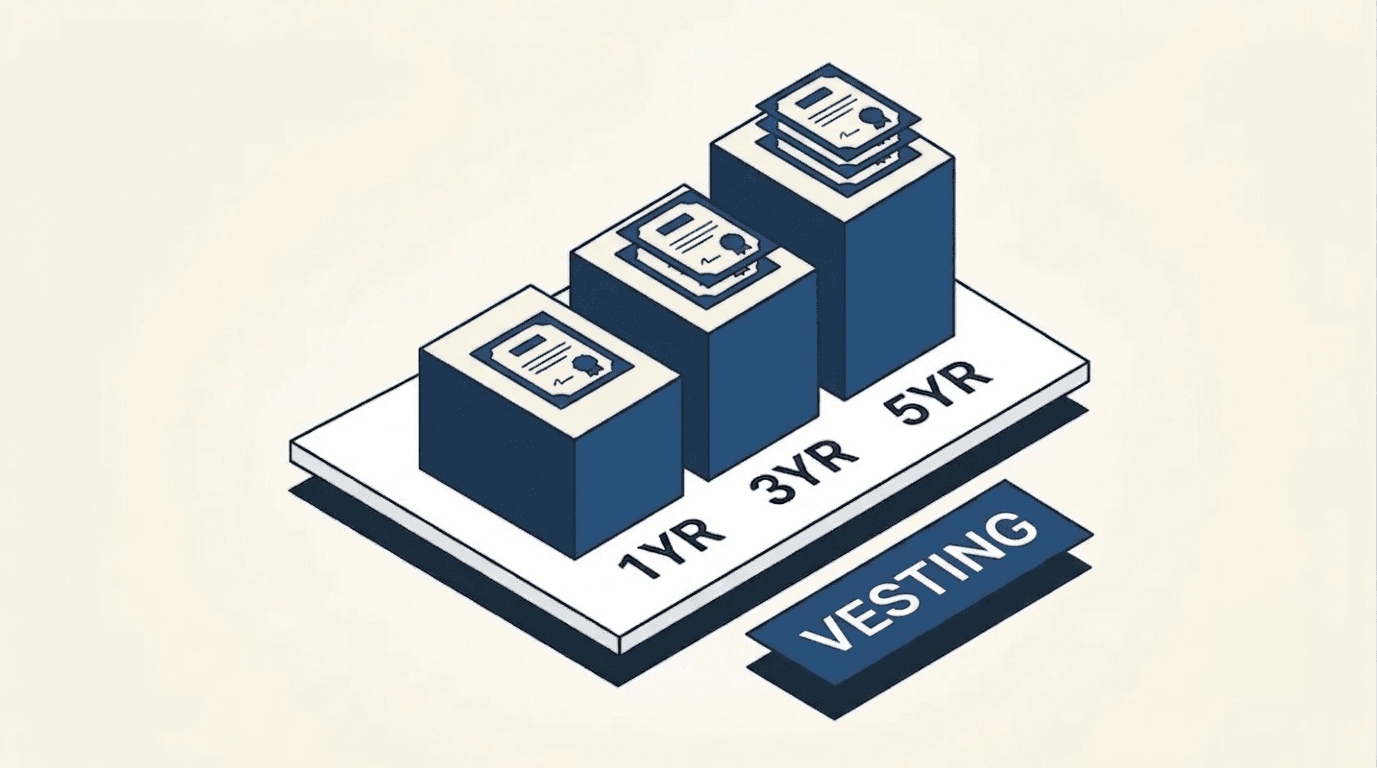

How RSU vesting works

RSUs are granted on a , commonly a four-year schedule with a one-year , followed by monthly or quarterly vesting after that. At a public company, each tranche that vests is delivered to you as shares (often minus a portion withheld to cover taxes) and can typically be sold immediately, subject to any around earnings.

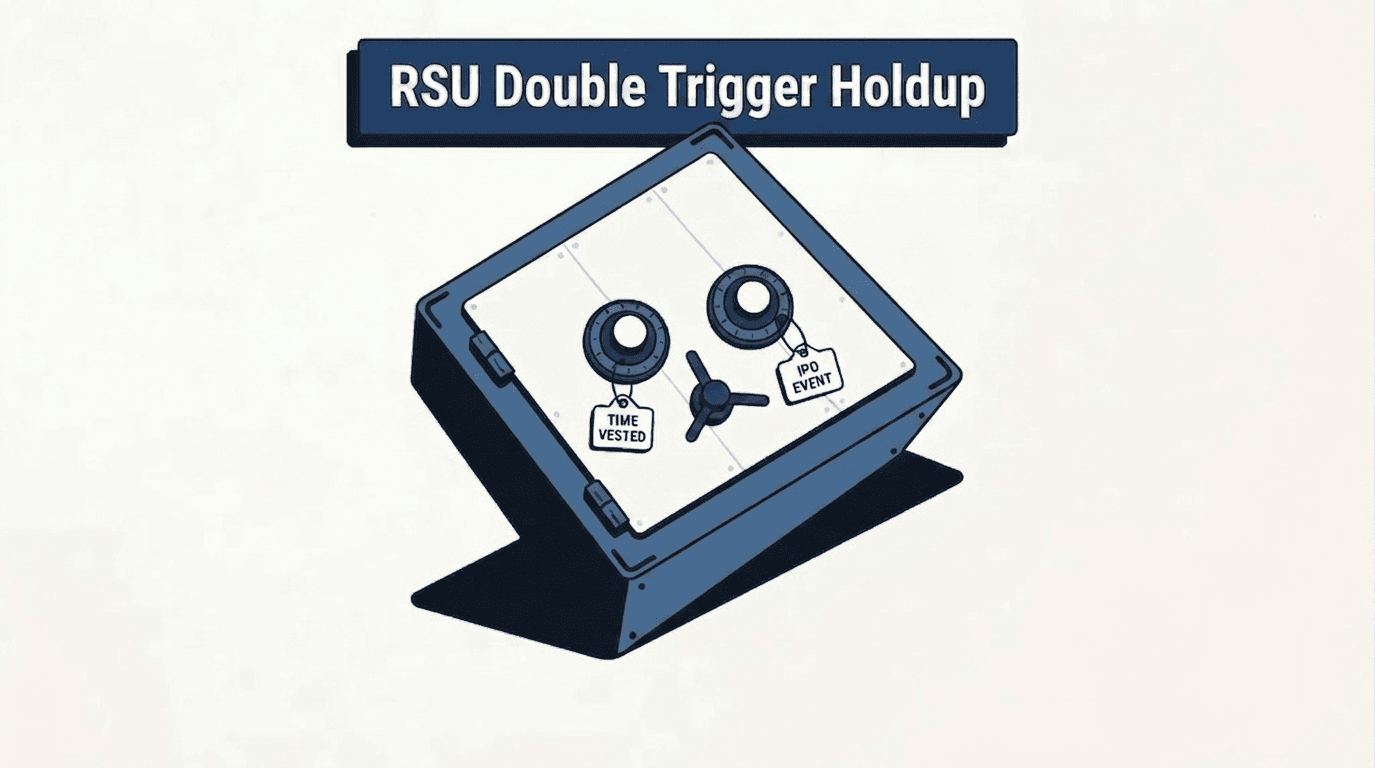

At a private company, RSUs frequently carry a second condition beyond time-based vesting: a liquidity event, such as an IPO or acquisition. Shares may vest on the calendar but not actually be delivered (and taxed) until that second condition is met, which is why some pre-IPO employees see large RSU tax bills concentrated around the company's public debut.

RSU tax treatment

RSUs are taxed as at vesting, based on the fair market value of the shares on the vest date. There is no tax at grant, and, unlike incentive stock options, RSU vesting does not trigger the alternative minimum tax. If you also hold ISOs alongside your RSU grants, it's worth modeling both together; you can estimate your AMT exposure from an ISO exercise with our calculator.

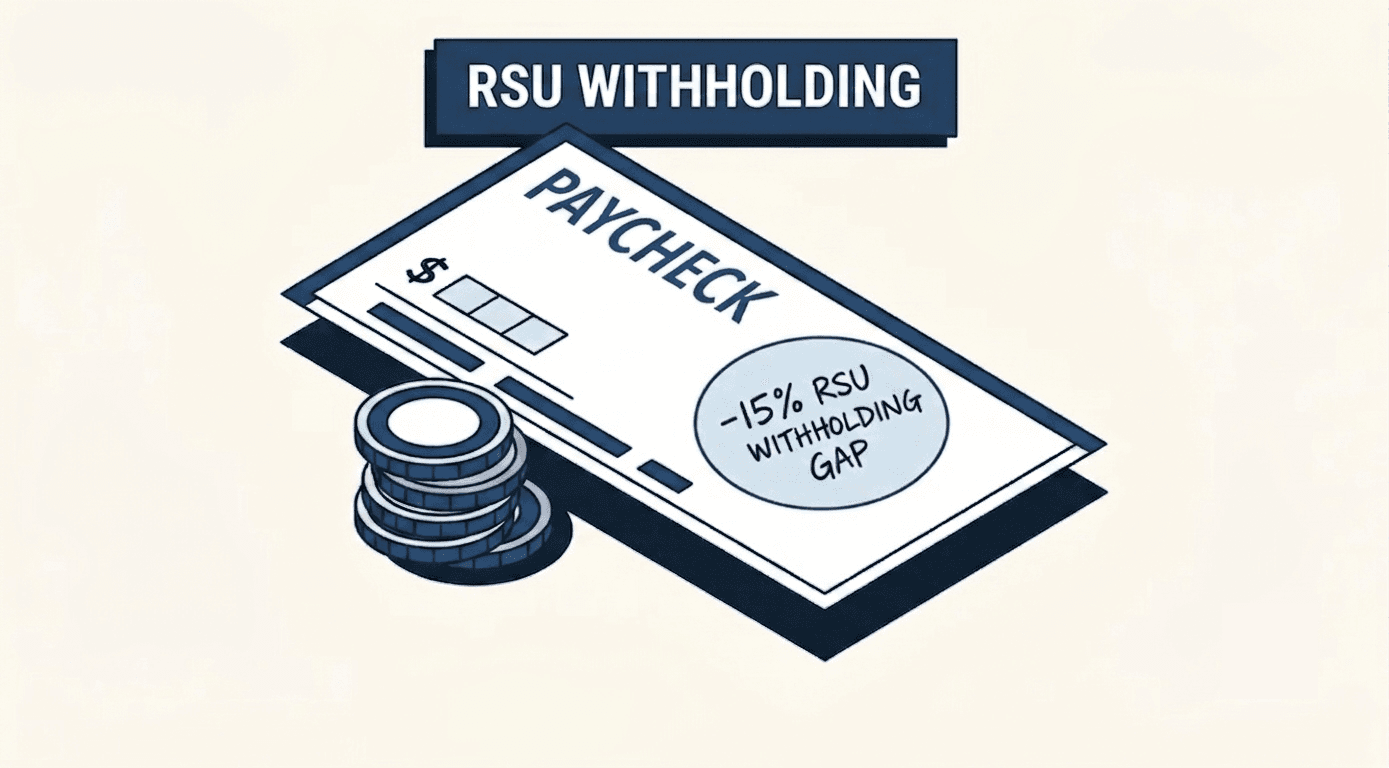

The withholding gap

Employers are required to withhold federal tax on RSU income at the flat : 22% on the first $1M of supplemental income in a year, 37% above that. The problem is that most tech professionals sit in the 32–37% marginal federal bracket, well above the 22% default. On a $100,000 vest, 22% withholding covers $22,000, but the actual federal tax owed at a 37% marginal rate is closer to $37,000, a $15,000 gap before state tax is even considered. Across several vests in a year, this shortfall can compound to $30,000–$80,000.

Left unaddressed, this gap becomes an April surprise, and if enough tax goes unpaid through the year, the IRS can add an underpayment penalty on top of the balance due.

Bracket creep on a large vest

Because RSU income stacks on top of your salary, a large vest can push your last dollars of income into a higher bracket than your base pay alone would suggest. This is one reason the same 22% withholding rate that's roughly right for a modest salary is rarely right for a senior engineer with a significant vesting schedule.

Cost basis and future gains

Once RSUs vest and the ordinary income tax is assessed, your cost basis in the shares resets to the fair market value at vesting. If you hold the shares afterward and they appreciate further, that additional gain is taxed separately, as a if held more than a year past vesting, or a short-term gain (taxed at ordinary rates again) if sold within a year.

A worked example: the withholding gap in dollars

Consider Nina, a hypothetical single filer and senior engineer who already earns $250,000 in salary. A $200,000 RSU tranche vests. Her employer withholds federal tax at the flat 22% supplemental rate, but that $200,000 stacks on top of her salary and lands in the 32% and 35% brackets.

Nina's $200,000 vest, step by step

- Federal withheld (22% flat)

- $44,000

- True federal tax on the vest

- ~$69,800

- Federal shortfall owed at filing

- ~$25,800

- Add state + Medicare, if not withheld

- up to ~$45,000+

The 22% rate sets aside $44,000, but Nina's true federal tax on the vest is closer to $69,800. That is a roughly $25,800 federal shortfall waiting at filing, and it holds in every state. Once state income tax and the additional Medicare tax are added, a client who is not separately covering them can owe well over $45,000 on a single vest. The fixes are straightforward once you see the number: raise your W-4 withholding, make a quarterly estimated payment, or sell enough shares at vest to fund the full bill.

Hypothetical, illustrative example. Nina is not a real client and these figures do not represent any actual client or outcome. Numbers are rounded and use approximate 2026 federal figures for a single filer; your result depends on your full tax picture and state. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Managing concentration risk

Every RSU tranche you hold rather than sell adds to your , the exposure created when a large share of your net worth sits in the same company stock that also pays your salary. A bad earnings quarter, or worse, can hit your income and your portfolio at the same time.

Holding vested RSUs is effectively a decision to use an after-tax cash bonus to buy more of your employer's stock. That can be a reasonable choice if you have high conviction and manageable concentration, but it's worth making that decision on purpose rather than by default, simply because selling requires an active step and holding doesn't.

A common approach is a systematic sell schedule that gradually moves shares into a diversified portfolio over 12–24 months, rather than an all-or-nothing choice at each vest.

The sell-vs-hold decision

At each vest, you generally have two choices: sell some or all of the shares immediately, or hold them. Selling at vest is a . Because your cost basis equals the vest-date value, there is little or no additional capital gain to report, and the proceeds can be used to cover the tax shortfall or diversify.

Holding instead means carrying continued price risk (and added concentration) in exchange for the possibility of further appreciation, plus eventual treatment if held more than a year past vesting. Which choice makes sense depends on your conviction in the company, how concentrated your overall portfolio already is, your near-term cash needs, and whether you're close to crossing the one-year holding threshold.

Building this rule in advance, before the shares vest and before a stressful market day, removes the emotion from the decision and keeps it consistent across every tranche.

RSUs vs. other equity types

Incentive stock options (ISO) and non-qualified stock options (NSO) are grants of the right to purchase stock at a fixed price, not outright grants of stock. You have to exercise them, and the tax treatment differs meaningfully from RSUs.

| RSU | ISO | NSO | |

|---|---|---|---|

| At vest / exercise | Ordinary income at vest (no purchase required) | May be subject to alternative minimum tax | May be subject to ordinary income tax |

| Sell | Capital gains on appreciation since vest | Ordinary income or capital gains | Capital gains |

Why the withholding rate matters more for RSUs

Because RSU income is taxed automatically at vest with no exercise decision to make, the withholding rate is effectively your only lever at the moment of the taxable event, and you can't choose to delay the tax the way you can sometimes time an option exercise. That's what makes the 22%-vs-marginal-bracket gap the central planning issue for RSU holders.

Common questions about RSU taxation

- RSUs are taxed as ordinary income at vesting (settlement), based on the fair market value of the shares on the vest date, added to your W-2 income. There is no tax at grant. The IRS applies a 22% supplemental withholding rate (37% on supplemental income above $1M in a year), which frequently leaves engineers in the 35–37% bracket underwithheld.

- Employers withhold federal tax on RSUs at the flat 22% supplemental rate, but most tech professionals sit in the 32–37% marginal bracket. On a $100,000 vest, 22% withholds $22,000 while you may actually owe about $37,000 federally, a $15,000 gap before state tax. Across several vests a year, the shortfall can reach $30,000–$80,000.

- Selling at vest (a same-day sale) converts concentrated company stock into cash, covers your tax, and removes further price risk. Your cost basis equals the vest-date value, so there is little or no capital gain. Whether to hold instead depends on your conviction, concentration, cash needs, and the one-year long-term capital gains threshold.

- No. RSUs vest as ordinary income and do not create an Alternative Minimum Tax preference item. AMT applies to incentive stock option (ISO) exercises, not RSU vesting. RSUs affect your regular tax liability, not your AMT calculation.

- Calculate your true marginal rate (federal + state + FICA), then close the gap before April: increase W-4 withholding, make quarterly estimated payments, or sell shares at vest to fund the full liability. In the vest year you can also reduce ordinary income by maxing your 401(k) and HSA, bunching deductions, or donating appreciated shares to a donor-advised fund.

Supplemental wage withholding rates per IRS Publication 15. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

Consult with an expert

Your RSUs are taxed at vesting whether you sell or not, and default withholding leaves a gap you owe in April.

Go over your equity, your broader financial goals, and see how the E.Q.U.I.T.Y. System™ can build a plan around them.

Book an Equity Strategy CallMore on Restricted Stock Units

Double-Trigger RSUs: Why Your Whole Tax Bill Hits at IPO

Double-trigger RSUs vest only when a time requirement and a liquidity event both happen. When your company IPOs, every year of vested shares lands as ordinary income at once.

How RSUs Are Taxed at Vesting: Why 22% Withholding Isn't Enough

RSUs are taxed as ordinary income the moment they vest, based on the full fair market value of the shares. The default 22% federal withholding often falls short of what higher earners owe, creating a tax bill due the following April.

Vesting Schedules Explained: Cliffs, Timing, and the Tax at Vest

Vesting turns a promised grant into owned equity on a schedule. RSUs are taxed as ordinary income the day each tranche vests, sold or not.

Important disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.