Double-Trigger RSUs: Why Your Whole Tax Bill Hits at IPO

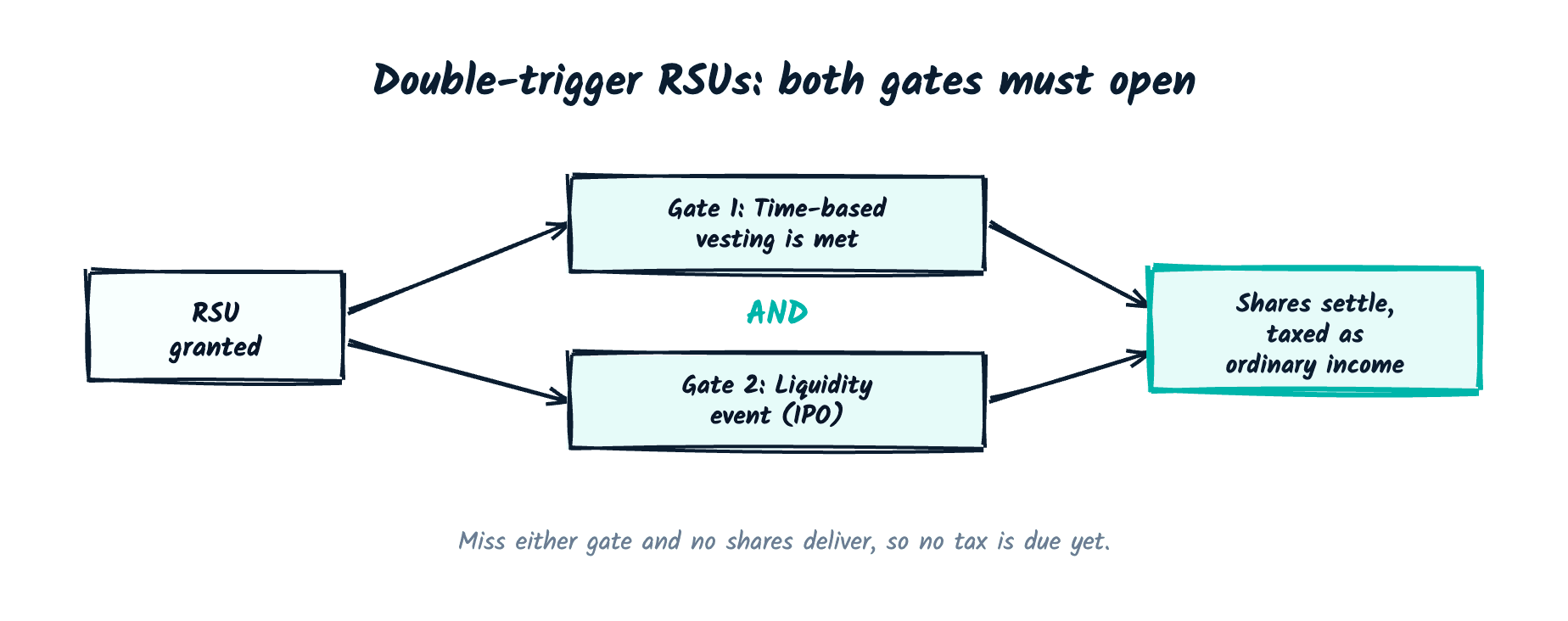

Double-trigger RSUs vest only when a time requirement and a liquidity event both happen. When your company IPOs, every year of vested shares lands as ordinary income at once.

A double-trigger RSU vests only when two conditions are both satisfied: a time-based schedule (usually four years) and a liquidity event, typically an IPO or acquisition. Until the second trigger fires, no shares vest and you owe no tax, no matter how long you've worked there. The day it fires, every year of time-vested shares can hit as ordinary income in a single tax return.

The two triggers explained

A single-trigger RSU vests on time alone: work four years, get your shares, pay tax on each vesting date as it happens. A double-trigger grant adds a second condition on top of that , and both have to clear before you own anything.

Private and pre-IPO companies use this structure for a practical reason. If they issued RSUs on a single trigger, employees would owe tax on shares of stock they can't sell, because there's no public market and no buyer for private company stock. Double-trigger vesting defers the tax event until the company goes public or gets acquired, at which point the shares (or cash, in an acquisition) become liquid enough to sell and cover the bill.

The two triggers work like this:

- Time-based vesting. Shares vest on a normal schedule, often 25% after a one-year and monthly or quarterly after that.

- Liquidity event. The company completes an IPO, direct listing, or acquisition, and (for IPOs) a lockup period typically expires 90 to 180 days later.

Both conditions must be met before a single share vests for tax purposes. An employee who has worked at a company for three years and cleared 75% of her time-based schedule owns zero taxable shares until the liquidity event occurs. If the company never goes public and never gets acquired, those shares can expire worthless when she leaves, even after years of vesting on paper.

Restricted stock at a public company vests and gets taxed on the same schedule the grant document lays out, with no second condition attached. Stock options work differently too: the grant sets an , and the employee chooses when to exercise. Double-trigger RSUs give the employee no control over timing at all. The company's IPO date sets the tax event for every employee holding this kind of grant at once.

Income stacking: why one event triggers years of tax

Every RSU tranche that already cleared its time-based schedule vests the day the liquidity event hits, and the IRS treats the full value as ordinary income earned in that one tax year. Four years of grants that would have been taxed gradually under a single-trigger structure instead land on one return.

Consider Priya, a staff engineer at Vantia Robotics, a pre-IPO defense-tech company. Priya joined four years before the IPO and received an initial grant plus two refresh grants along the way. By the time Vantia lists publicly, she has cleared the time-based portion of all three grants: 60,000 shares total. Vantia prices its IPO at $40 per share. On the day the second trigger fires, Priya's income tax return has to account for $2,400,000 of ordinary income, all in a single year, even though those shares represent four years of work.

This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

That $2.4 million pushes Priya from whatever bracket her base salary would put her in straight into the top federal bracket, plus the additional Medicare tax, plus, depending on her state, a state income tax bill calculated on the same lump sum. None of this reflects a bad decision on her part. It's a mechanical consequence of how the company structured the grant from day one.

Think of it like a reservoir behind a dam. A single-trigger grant releases water on a steady schedule, a little every quarter, so the river downstream never floods. A double-trigger grant holds everything back until the dam opens once, and four years of water arrive on the same day. The total volume hasn't changed. The timing has, and timing determines whether the riverbank can absorb it without damage.

The withholding gap this creates

Employers withhold RSU income at the flat federal : 22% for the first $1 million of supplemental income in a calendar year, 37% above that. Anyone whose marginal rate sits above 22%, and after a large stacked vest that describes most people in this situation, gets less withheld than they owe.

Run Priya's numbers. On $2,400,000 of stacked RSU income, her employer withholds 22% on the first $1,000,000 ($220,000) and 37% on the remaining $1,400,000 ($518,000), for total withholding of $738,000. Once that income combines with her salary and runs through the full progressive bracket structure, plus any Medicare surtax, her actual federal liability lands above the $738,000 withheld. How far above depends on her filing status, deductions, and state: exactly the kind of number to model with an advisor or the RSU Tax Withholding Calculator before the vest date, not estimate with a rule of thumb. Whatever the final figure, the shortfall comes due the following April, and it surprises employees who assumed withholding meant "already paid."

Withholding is not a tax calculation. The 22%/37% supplemental rate is a flat administrative default, not a projection of what you owe. Payroll systems apply it because it is easy to run, not because it matches your bracket.

Sell-to-cover doesn't fix the gap. Most plans withhold shares at the same flat supplemental rate, so a sell-to-cover election still leaves the same underpayment sitting on your return.

State withholding compounds the problem. High-tax states often withhold RSU income at a flat rate too, which can fall well short of your actual state marginal rate on a stacked vesting event.

If your RSUs vest at a company already covered in our piece on how RSUs get taxed at vesting, the mechanics of the single-trigger case are the same withholding math applied to smaller, annual amounts. Double-trigger vesting just concentrates four years of that same math into one date.

Lockup periods add a liquidity mismatch

A standard IPO lockup agreement prevents employees from selling shares for 90 to 180 days after the offering, even though the shares vested (and became taxable) on the IPO date itself. That creates a window where the tax bill comes due but the shares that would fund it can't be sold.

Priya owes tax on $2.4 million of income the day Vantia lists, but her lockup runs 180 days. Vantia's stock drops 30% during that window, a common pattern once early investors and employees who can sell start doing so. Priya still owes tax calculated on the IPO-day value, not the lower price she can sell at once the lockup lifts. She's also carrying enormous : a large share of her net worth sits in one stock she can't touch and can't hedge during a that typically overlaps with the lockup.

A large tax bill due immediately, paired with an illiquid, concentrated position for months afterward, is the central planning problem of double-trigger RSUs. We cover it in more depth in our article on managing concentration risk after a liquidity event.

Planning moves before the liquidity event

Once you know your company is heading toward an IPO or acquisition, a few moves are worth evaluating before the second trigger fires.

Estimate the stacked income now, not later. Add up every tranche that has cleared or will clear its time-based schedule by the expected liquidity date, then model the tax at your actual marginal rate rather than the 22% withholding default.

Set aside cash outside the position. Build a reserve from salary or bonus that doesn't depend on selling company stock, since you may not be able to sell shares during the lockup even if the tax bill arrives first.

Check your withholding elections where the plan allows it. Some employers let you elect additional withholding beyond the flat statutory rate. If yours does, this is the year to use it.

Coordinate timing with other pre-IPO moves. If you also hold ISOs or QSBS-eligible stock at the same company, the year a huge RSU stack lands is exactly the year those decisions need advance planning rather than a scramble.

We walk through the fuller sequence of decisions, ISO exercise timing, QSBS eligibility checks, 83(b) windows on early-exercised shares, in our guide to pre-IPO planning moves. The earlier you model this, the more choices you have.

Planning moves after the liquidity event

Once the shares vest and the lockup starts running, the priority shifts from avoiding the tax bill, which you can't, to managing the cash and the concentration that follow it.

| Timing | Action | Why it matters |

|---|---|---|

| Vest date | Confirm actual withholding vs. estimated liability | Catches the gap before quarterly estimates are due |

| Within 30-45 days | File or adjust quarterly estimated payments | Avoids IRS underpayment penalties on the shortfall |

| During lockup | Build a diversification plan for when shares free up | Sets a plan instead of reacting to price swings |

| Lockup expiration | Execute a staged sale, not an all-at-once dump | Reduces timing risk and signals discipline to the market |

A same-day, all-shares sale the moment the lockup lifts is rarely the right call. Holding everything indefinitely out of loyalty to the stock isn't either. Most employees land somewhere in between: sell enough to cover taxes and reduce concentration to a level they can sit with, then hold a smaller position if conviction and risk tolerance support it.

For the pillar-level view of how RSUs work across grant, vest, and sale, start with our RSU basics guide, then use this article's mechanics to model your specific liquidity event.

Common questions

No. Public companies almost always use single-trigger RSUs, since a public market already exists to make shares liquid and taxable at each vesting date. Double-trigger structures exist to solve the private-company problem: no market to sell into and no cash to pay tax with. Once a company completes its IPO, new grants issued afterward typically revert to single-trigger vesting on a normal schedule.

You forfeit them. Both conditions must be met, and since the liquidity event hasn't happened yet, shares that have only cleared the time-based portion carry no vested value and no ownership. This is a real risk for anyone who leaves a pre-IPO company mid-career, and it's one reason concentrated equity in a single private employer carries more risk than a steady paycheck and a rising 401(k) balance might suggest.

Selling right after vesting doesn't reduce the ordinary income tax already triggered at vest, because the value on the vesting date fixes that liability regardless of what you do next. An immediate sale locks in that value and generates cash to cover the bill, which matters given how much concentrated stock can swing during and after a lockup period. Any gain or loss after vesting is a separate, smaller capital gains calculation, taxed on the difference between the vest-date value and the sale price.

Last updated: July 2026. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Consult with an expert

An IPO can stack years of RSU tax into a single return. Plan the hit before it lands.

No commitment. A clear read on your situation from a CFP® who plans equity compensation for a living.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

This article is for educational purposes only and reflects rules in effect as of the date above. Tax figures are estimates. Consult a qualified tax or financial advisor for advice specific to your situation.

Get the next article in your inbox.

No fluff. Just equity strategy and tax clarity, when it matters.

Keep reading

Restricted stock units (RSU)

How RSUs are taxed at vesting and why default withholding leaves a gap.

Read the guideESPPEmployee stock purchase plan (ESPP)

Buy company stock at a ~15% discount, a return most eligible employees never claim.

Read the guideCalculatorAMT Safe-Exercise Calculator

Holding options too? See your AMT exposure before you exercise.

Read the guideImportant disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.