Concentration Risk: When Your Net Worth Rides on One Stock

Concentration risk is holding so much of one company's stock that a single decline could derail your financial plan. Learn the 10-20% rule of thumb, the tax cost of selling, and how staged diversification works.

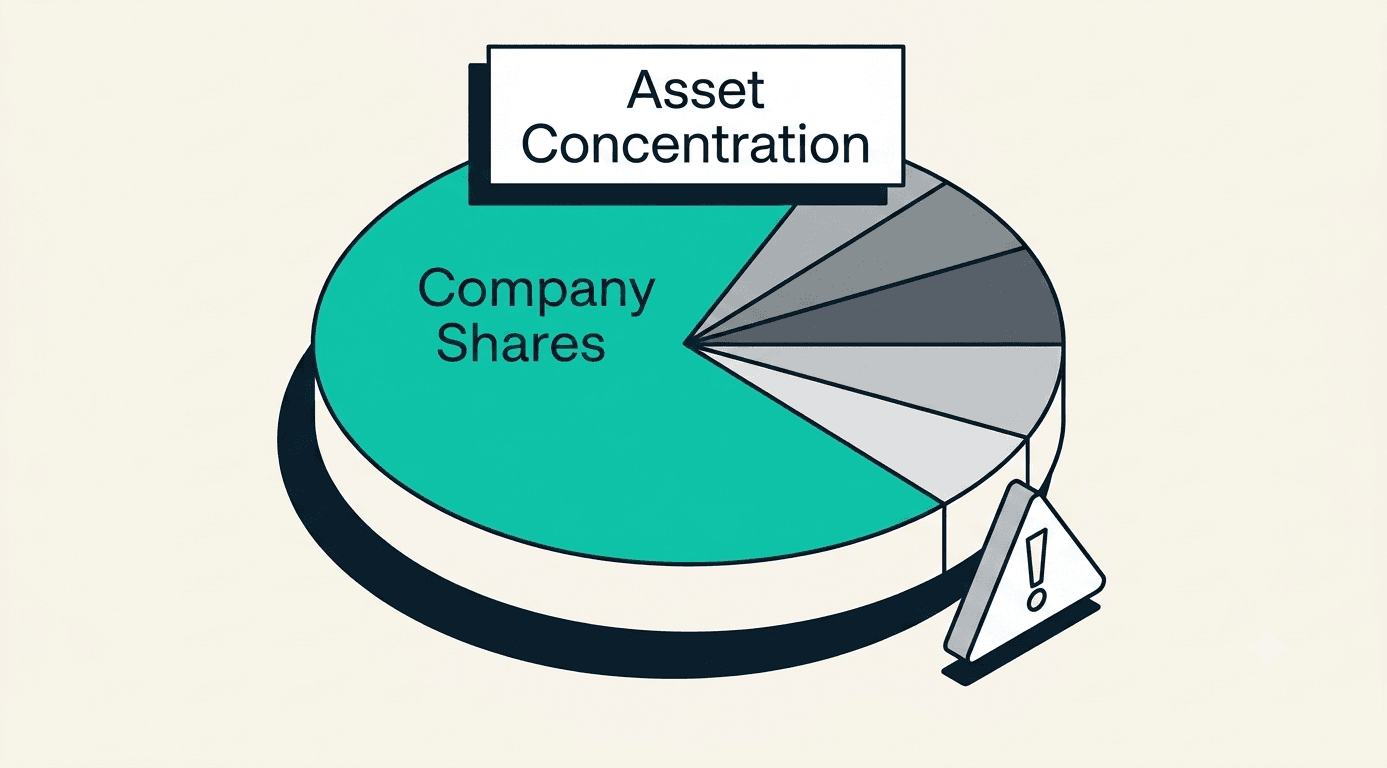

Concentration risk means holding so much of one company's stock, through and exercised options, that its performance now drives your financial future more than your own savings rate or asset allocation does. Most advisors flag a problem once a single stock crosses 10-20% of net worth. Past that line, you carry risk you never chose and no market pays you to hold.

What Counts as Concentration Risk

A position counts as concentrated once it can move your net worth up or down by a meaningful percentage on its own, independent of your job performance or your broader portfolio. The common threshold planners use is 10% of investable net worth as a caution flag and 20% as a point where most people need an active plan, not just awareness.

For an employee at a public company, this usually means unvested and vested RSUs plus any ISOs or NSOs exercised and held. For someone at a private company, the number includes the current of vested shares, which can swing hard between funding rounds and carries no public market to sell into even if you wanted out.

Take Dana, a senior engineer at Solace Health, a pre-IPO health-tech company. Dana joined four years ago, has fully vested her original grant, and received two refresh grants since. Her 409A-priced equity is currently worth $1.4 million against a total net worth of $1.7 million, once retirement accounts and a small brokerage account are included. Solace stock is roughly 82% of everything Dana owns. If Solace's next valuation resets down, as happened to several peers in her space in 2022, Dana's net worth falls with it, and she has no way to sell private shares to cushion the drop.

Why This Risk Goes Uncompensated

Diversified portfolios earn a risk premium because investors get paid, on average, for holding market-wide exposure. A single stock does not offer that same deal. You take on , meaning the chance that one company's outcome, not the broader economy, determines your financial security, and the market does not pay extra for it. Academic research on idiosyncratic (single-company) risk consistently finds no reliable long-run premium for it, since any investor can diversify that risk away for free by not concentrating in the first place.

The risk also compounds in an uncomfortable way for equity comp employees. Your paycheck, your bonus, your 401(k) match, and your equity all come from the same employer. A downturn that hits your company's stock price often coincides with layoffs, hiring freezes, or reduced 409A valuations at private companies. Dana's income, career trajectory, and net worth all move together. That correlation is the part a rule of thumb like "10-20% of net worth" is trying to protect against.

Employer overlap. Salary, bonus, retirement match, and equity value all depend on the same company's fortunes, so a bad quarter can hit every income stream at once.

No public exit for private shares. Pre-IPO employees often cannot sell vested shares outside of tender offers, leaving concentration risk fully exposed between liquidity events.

Behavioral anchoring. Employees who watched their stock triple often assume the trend continues, which delays diversification until after a decline instead of before one.

The Tax Tail on Selling

Selling concentrated stock triggers a tax bill that depends entirely on how you got the shares and how long you have held them. RSU shares vest as at fair market value, and your cost basis resets to that vest-day price. Sell RSU shares soon after vesting and you typically owe little beyond what was already withheld, since there has been almost no price movement to tax.

ISOs and NSOs work differently. Shares from an ISO exercise held past the vest date can qualify for treatment if you clear the one-year-from-exercise and two-year-from-grant holding periods. Sell before that window closes and you trigger a , which reclassifies the gain as ordinary income in the year of sale. Exercising ISOs early enough to start that clock can also trigger the alternative minimum tax in the exercise year, because the spread between exercise price and fair market value counts as AMTI even though no cash changed hands. The AMT calculator models that exposure before you exercise, using your specific grant numbers rather than a rule of thumb.

This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

For 2026, the AMT exemption is $140,200 for married filing jointly and $90,100 for single filers. It phases out starting at $1,000,000 of income (MFJ) or $500,000 (single) at 50 cents per dollar, which pushes the effective marginal rate in that band to roughly 42%. A large ISO exercise timed poorly can land squarely in that phaseout zone. That is exactly the kind of number an employee sitting on concentrated equity needs modeled before exercising, not after.

Diversification Moves That Work

The most reliable diversification tactic is a sell-at-vest default: route newly vested RSU shares to cash or a diversified account as soon as they land, rather than letting them accumulate. Since RSU shares carry almost no unrealized gain at vest, selling immediately locks in minimal tax cost and keeps the position from growing larger every quarter. Employees who wait, hoping for further upside, are the ones who show up years later at 60-80% concentration with a much larger tax bill on any gain.

For employees at public companies who face or insider-trading restrictions, a 10b5-1 trading plan solves the timing problem. You set a predetermined selling schedule while you have no material nonpublic information, and the plan then executes automatically during blackout windows without any real-time decision-making on your part. This removes both the compliance risk and the emotional temptation to time the stock.

Where a position built up gradual gains, whether from long-held RSUs or exercised options, staged selling over multiple tax years spreads the capital gains recognition and avoids pushing a single year into a higher bracket or an AMT phaseout band. A common approach sells a fixed percentage of the position, or a fixed dollar amount, on a quarterly schedule regardless of price, which also removes the guesswork of trying to pick a top.

Sell-at-vest default. Route new RSU vests to cash or a diversified fund immediately, since the tax cost is lowest right at vesting and the position never gets larger than it needs to.

10b5-1 plans for public companies. Pre-set a selling schedule while unrestricted, then let it run automatically through blackout periods without further input.

Staged selling across tax years. Sell fixed increments on a schedule to spread gains, avoid AMT phaseout exposure, and stop trying to guess a peak price.

Holding 80% of your net worth in one employer's stock resembles insuring your house, your car, and your health all through the same small insurer. If that insurer fails, every policy fails at once. Diversification means buying coverage from more than one source.

For a fuller walkthrough of what happens the moment shares vest, see how RSUs get taxed at vesting. Our RSU learning center guide covers vesting schedules, withholding, and sale timing in full. And if your equity sits at a private company still working toward an exit, pre-IPO planning moves covers the sequencing questions that come before any of this, including tender offers and secondary sales.

QSBS Awareness Before You Sell

Before selling concentrated shares in a private company, check whether they qualify for the exclusion under Section 1202. A full or partial capital gains exclusion changes the diversification math substantially. Shares acquired on or before July 4, 2025 follow the legacy rule: a 100% exclusion once you clear a full five-year hold, all-or-nothing, capped at the greater of $10 million or 10x basis, and the issuing company had to meet a $50 million gross-assets test at the time of issuance.

Shares acquired after July 4, 2025 follow a tiered schedule under the One Big Beautiful Bill Act: 50% exclusion at a three-year hold, 75% at four years, and 100% at five years. The cap rises to $15 million, indexed for inflation after 2026, and the gross-assets test at issuance rises to $75 million. Any portion of the gain not excluded is taxed at a flat 28% QSBS rate rather than ordinary long-term capital gains rates.

California does not conform to the federal QSBS exclusion and taxes the full gain regardless of which regime applies. That matters for any employee at a California-headquartered startup planning to relocate before a sale. For an employee who needs liquidity before the holding period completes, Section 1045 allows a rollover into replacement qualified stock if the original shares are held at least six months and the proceeds are reinvested within 60 days, preserving QSBS eligibility on the deferred gain.

None of this changes the underlying diversification math for the diversifiable, taxable portion of a position. It changes the sequencing. An employee close to a three, four, or five-year QSBS anniversary has a real reason to hold a few more months rather than sell into full ordinary tax treatment on shares that would otherwise qualify for partial or full exclusion.

Common questions

Most planners flag 10% as a caution point and 20% as a threshold requiring an active diversification plan. There is no single correct number, since risk tolerance, age, and other assets all matter. Once one employer's stock can single-handedly move your net worth by double-digit percentages, that concentration is worth addressing deliberately rather than by default.

Waiting concentrates the position further and adds more unrealized gain, which raises the eventual tax bill without adding any diversification benefit in the meantime. A stock that has already outperformed is statistically no more likely to keep outperforming than any other stock, and the downside of a decline grows every month the position stays uncut.

It depends on the source. RSU shares sold near vesting carry minimal embedded gain since basis resets at vest. ISO or NSO shares held for gains, or private QSBS-eligible shares, can carry a much larger tax cost or a much larger benefit depending on holding period and exclusion eligibility. Model the specific lot before selling rather than assuming one tax outcome applies to all shares.

Last updated: July 2026. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Consult with an expert

When your paycheck and your portfolio ride the same stock, one drop takes both.

No commitment. A clear read on your situation from a CFP® who plans equity compensation for a living.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

This article is for educational purposes only and reflects rules in effect as of the date above. Tax figures are estimates. Consult a qualified tax or financial advisor for advice specific to your situation.

Get the next article in your inbox.

No fluff. Just equity strategy and tax clarity, when it matters.

Keep reading

Incentive stock options (ISO)

Start with how ISOs are taxed and where AMT comes from.

Read the guideRSURestricted stock units (RSU)

How RSUs are taxed at vesting and the withholding gap to plan around.

Read the guideCalculatorAMT Safe-Exercise Calculator

Run the numbers on an ISO exercise before year-end.

Read the guideImportant disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.