QSBS: How to Exclude $10M to $15M in Gains

Section 1202 lets founders and early employees exclude some or all of the gain on qualified small business stock. Here is how the exclusion works under both the pre and post July 2025 rules.

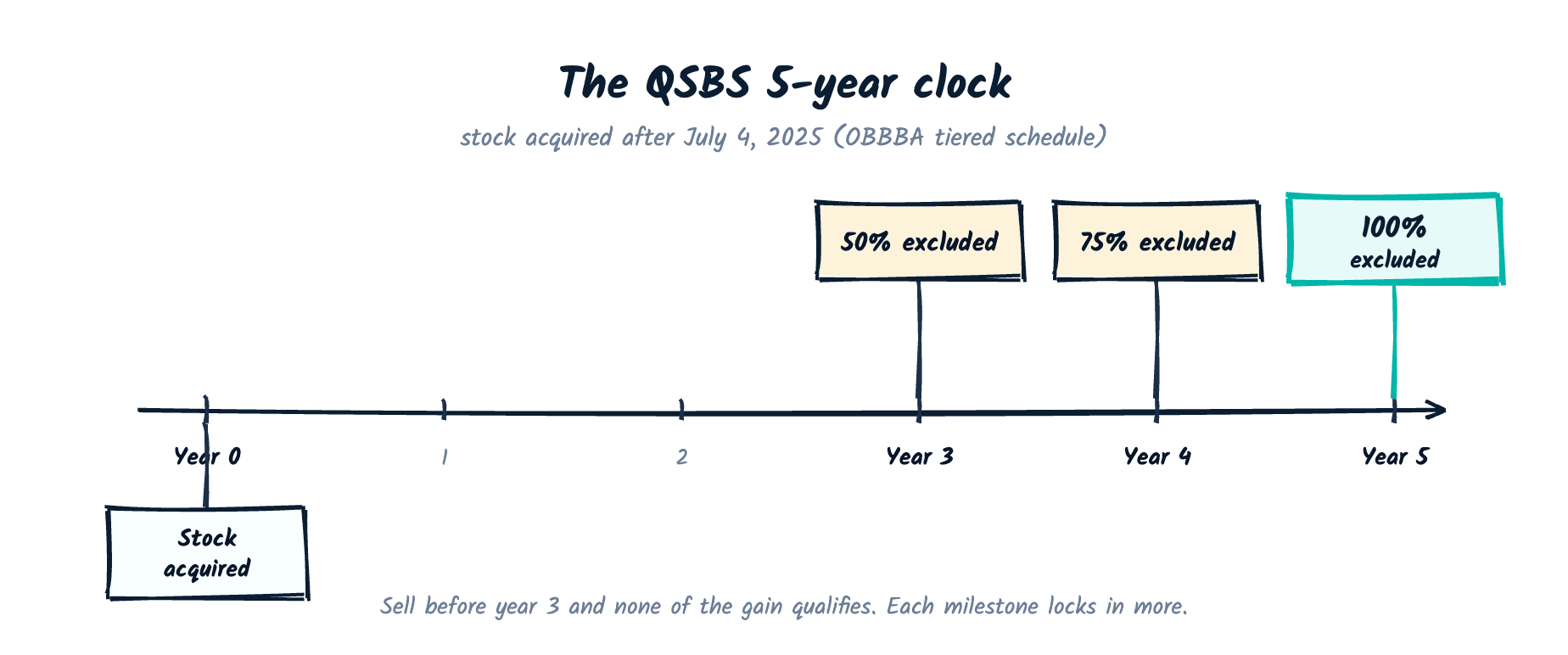

Section 1202 of the tax code lets you exclude some or all of the gain when you sell qualified small business stock. Stock acquired on or before July 4, 2025 can exclude 100% of gain up to the greater of $10 million or 10 times basis, once you clear a five-year hold. Stock acquired after that date follows a tiered schedule capped at $15 million, with partial exclusions starting at year three.

What Qualifies as QSBS

is stock issued directly by a domestic C corporation to you, in exchange for cash, property, or services, at a time when the company's gross assets stayed under the statutory threshold. You have to be the original holder. Stock you bought from another employee on a secondary market, or bought through a private sale on a platform like Forge or EquityZen, does not qualify, even if the underlying company otherwise meets every test.

The company also has to run an active trade or business. Investment vehicles, holding companies, and certain service businesses (law, accounting, consulting, financial services, health, and a handful of others) are excluded by statute. Most venture-backed technology and biotech companies clear this bar without issue, but a company that pivots into holding investments or licensing IP passively can lose eligibility going forward. Read our full QSBS pillar guide for the complete list of excluded businesses.

Most employees never think about QSBS until a term sheet lands or an acquirer starts due diligence. By then the eligibility questions are mostly answered by facts already in the past: when the stock was issued, what the company's balance sheet looked like at that moment, and whether you bought the shares directly or picked them up from someone else. None of that can be fixed retroactively, which is why the analysis belongs earlier in your planning, ideally the year you join a company or exercise options, not the year you plan to sell.

Restricted stock units complicate this picture. RSUs settle in shares only at vesting, and the shares you receive are typically treated as issued to you at that later date, not at your original grant date. That can push your holding period start much later than someone who early-exercised stock options and filed an 83(b) election on day one. If your compensation mixes options and RSUs, treat each grant separately for QSBS purposes rather than assuming one clock covers everything you hold.

The Two Regimes: Before and After July 4, 2025

The One Big Beautiful Bill Act rewrote Section 1202 for stock acquired after July 4, 2025, and left the old rules in place for anything acquired on or before that date. Your acquisition date, not your sale date, decides which regime applies.

| Acquired on/before July 4, 2025 | Acquired after July 4, 2025 | |

|---|---|---|

| Hold period for exclusion | 5 years, all or nothing | Tiered: 50% at 3 years, 75% at 4 years, 100% at 5 years |

| Exclusion cap | Greater of $10M or 10x basis | $15M, indexed for inflation after 2026 |

| Gross-assets test at issuance | $50M | $75M |

| Tax on the non-excluded portion | Standard rates | Flat 28% QSBS rate |

The practical effect: employees who received stock years ago under an early grant still get the older, simpler all-or-nothing structure. Anyone receiving new grants or making new investments today falls under the tiered regime, which rewards an earlier exit but caps the benefit at a lower dollar figure on a very large gain.

Meeting the Eligibility Tests

Four conditions have to hold at once for a share of stock to qualify. Miss any one and the exclusion disappears for that block of shares.

Original issuance only. You must acquire the stock directly from the corporation, not from a departing employee or a secondary marketplace. Shares received through an on early-exercised options count as original issuance.

Gross assets test. The corporation's gross assets, measured immediately after your stock is issued, cannot exceed $50 million (legacy) or $75 million (post July 2025). This is tested once, at issuance, not at sale.

Active business requirement. At least 80% of the company's assets have to be used in an active trade or business, and that business cannot fall into the excluded categories under the statute.

C corporation status. The company has to be a domestic C corporation both when the stock is issued and substantially throughout your holding period. LLCs and S corporations do not issue QSBS.

Marcus, a product manager at Halyard Systems, a pre-IPO logistics software company, early-exercised his ISOs the month he joined and filed an within the 30-day window. That single filing started his QSBS clock at grant date rather than at vesting, four years earlier than if he had waited. Early exercise also triggers an AMT calculation in the exercise year, since the spread between his and counts as an AMT preference item even at a low 409(a) valuation. He ran the numbers before filing.

Free tool

Know your AMT exposure before you exercise

Early exercising ISOs to start your QSBS clock can still trigger an AMT bill. Model your specific numbers before you file the 83(b).

Run the AMT calculator

If you're weighing early exercise for QSBS purposes, our piece on deciding when to exercise ISOs walks through the tradeoff in more depth.

How Much You Can Exclude

The exclusion cap is the larger of two numbers: a flat dollar figure or a multiple of your basis. For legacy stock, that means the greater of $10 million or 10 times your basis in the shares. For stock acquired after July 4, 2025, the flat figure rises to $15 million, and Congress built in inflation indexing starting in 2027.

This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Consider Dana, an early engineer at Corvalt Systems, a pre-IPO fintech company, who received founder-adjacent stock in 2020 with a basis of $150,000. By 2026 her stake is worth $11 million at exit, a $10.85 million gain. Her 10x-basis figure is $1.5 million, well below the $10 million flat exclusion, so her cap is $10 million. She excludes $10 million of gain federally and pays capital gains tax on the remaining $850,000.

Now compare Raj, who joined the same company in September 2025 after the OBBBA cutoff. His shares carry the tiered schedule and a $15 million cap. If he sells at the four-year mark, he excludes 75% of gain up to that cap; anything above the cap, and the non-excluded 25% below it, gets taxed at the flat 28% QSBS rate rather than ordinary capital gains rates. Waiting one more year to hit the five-year mark converts that 75% into a full 100% exclusion, a difference worth modeling if a liquidity event is close.

The California Trap

California does not conform to Section 1202. The state taxes the full gain under its own rules, regardless of what you exclude on your federal return. An employee who moves to California before selling, or who has always lived there, should assume the full gain is taxable at the state level even after a clean federal exclusion.

This catches people by surprise: the federal return shows a clean exclusion, and the state return does not. If you're planning a sale timed around a QSBS hold period, or considering a change of residency before a liquidity event, run the state-level numbers separately and well in advance. Several other states also decouple from federal QSBS treatment, so check your specific state rather than assuming conformity.

Timing a residency change around a sale raises its own set of rules around domicile, days spent in-state, and where your income is considered sourced, and those rules vary by state and get scrutinized closely when large gains are involved. A move made purely for tax reasons, executed close to a liquidity event, invites exactly the kind of audit attention state tax authorities are trained to look for. Anyone considering it should loop in a tax attorney who works across state lines well before signing anything related to the sale.

Rolling Gains Forward with a 1045 Exchange

A Section 1045 rollover lets you defer gain on QSBS sold before you clear the full holding period, as long as you held the original stock more than six months and reinvest the proceeds into new QSBS within 60 days of the sale. This matters most when a company gets acquired early, before your five-year (or three-year, under the tiered regime) clock runs out, and you'd otherwise lose the exclusion entirely on that block of shares.

The rollover doesn't forgive the gain. It defers it and lets your original holding period carry over into the replacement stock, so the clock keeps running rather than resetting. This is one of the moves worth mapping out before a deal closes rather than after, alongside other pre-IPO planning moves that depend on timing you control only up to a point.

The 60-day reinvestment window is tighter than it sounds once an acquisition closes. Wire transfers, escrow releases, and the paperwork around a new investment can eat two or three weeks before you've even identified a replacement company. Employees who expect their company to get acquired before they clear five years should start scouting realistic 1045 replacement investments ahead of the deal, not after the closing wire hits their account. A financial advisor and a tax attorney working together can identify qualifying replacement stock and confirm the mechanics before the clock starts running.

A 1045 rollover only defers the portion of gain tied to stock that hasn't yet cleared its holding period. If part of your position already qualifies for full exclusion at sale, roll only the remainder forward. Separating a mixed position into "already qualifies" and "still needs the rollover" pieces before you sell keeps the analysis clean and avoids rolling forward gain you could have excluded outright.

Common questions

No. Section 1202 only applies to stock issued by a domestic C corporation. Membership interests in an LLC, even one taxed favorably, and shares in an S corporation never qualify as QSBS, regardless of how small or early-stage the business is. If your company operates as an LLC today and plans to convert to a C corporation later, only stock issued after that conversion can start a QSBS clock.

The gross assets test and your holding period both start at the date the company issues you C-corp stock, not at the date you joined the LLC. A conversion from LLC or S-corp to C-corp creates a fresh issuance for QSBS purposes, so your five-year (or tiered) clock begins on the conversion date, and the applicable gross-assets threshold depends on when that conversion happens relative to July 4, 2025.

Yes. The exclusion cap applies per issuer, per taxpayer, not as a single lifetime limit across your whole portfolio. If you hold qualifying stock in three different companies and each sale meets the holding period and gross-assets tests, you can claim a full exclusion, up to each company's own cap, on each separate sale. Married couples filing jointly generally each get their own cap as well, though the mechanics depend on how the stock is titled.

Last updated: July 2026. This is an estimate only. Consult a qualified tax or financial advisor for personalized advice.

Consult with an expert

One early sale or paperwork miss can erase a seven-figure QSBS exclusion. The rules are unforgiving.

No commitment. A clear read on your situation from a CFP® who plans equity compensation for a living.

Author

Mitchell Ludwig, CFP®Mitchell built his practice around one problem: helping tech professionals turn equity compensation into lasting wealth. A decade guiding engineers through ISO exercises, AMT exposure, and liquidity events — no generic advice, no handoffs.

This article is for educational purposes only and reflects rules in effect as of the date above. Tax figures are estimates. Consult a qualified tax or financial advisor for advice specific to your situation.

Get the next article in your inbox.

No fluff. Just equity strategy and tax clarity, when it matters.

Keep reading

QSBS: the founder tax exclusion

How qualified small business stock can exclude up to 100% of gain from federal tax.

Read the guideISOIncentive stock options (ISO)

How ISOs are taxed and how the exercise interacts with a future QSBS holding period.

Read the guideCalculatorAMT Safe-Exercise Calculator

Estimate the AMT cost of exercising early to start your QSBS clock.

Read the guideImportant disclosures

Mitchell Ludwig is a CERTIFIED FINANCIAL PLANNER™ professional and a Registered Investment Adviser Representative of Carolina Wealth Partners. Securities are offered through United Planners Financial Services, Member FINRA/SIPC. Carolina Wealth Partners and The Equity Architect are separate entities. Jon Ludwig is a Series 65–registered Investment Adviser Representative and promoter.

All content on this page is for informational and educational purposes only and does not constitute personalized investment, tax, or legal advice. Examples, illustrations, and client archetypes are composite in nature and do not represent any specific client. All tools and calculators are estimates only. Consult a qualified tax advisor or CFP® professional before making any financial decisions.

All marketing content is reviewed and approved by United Planners compliance in accordance with SEC Marketing Rule (Rule 206(4)–1). Past performance is not indicative of future results.